The Raw Steels Monthly Metals Index (MMI) moved sideways amid bearish steel prices, with a modest 1.75% increase from February to March. U.S. flat rolled steel prices stayed bearish over the past few weeks. Meanwhile, HRC prices remained 22% beneath their peak at the close of 2023 as they search for a new bottom. However, […]

Category: Ferrous Metals

JSW Steel Aiding Italy’s Steel Industry with €140 Million Investment

One of India’s fastest-growing steel companies JSW Steel, recently announced the next step in its growth plan. In a major steel news event, JSW Steel Italy SRL inked a memorandum of understanding (MoU) with the Italian government to re-start production operations at the Piombino plant via a €140 million investment. According to JSW Steel, the […]

Construction MMI: Potential Manufacturing Boom Could Impact Steel Prices

Month-over-month, the index experienced little movement. Overall, the Construction MMI (Monthly Metals Index) moved sideways, inching down just 1.2%. Steel prices moving downward placed some bearish pressure on the index. However, several significant factors continue to press on construction from both a bearish and bullish standpoint, including the Fed holding off on adjusting interest rates, […]

Automotive MMI: Automotive Market Improves, but Bears Show Up for Steel Prices

Month-over-month, the Automotive MMI (Monthly Metals Index) dropped by 3.03%. While the automotive market continued to improve overall, bearish pressure on certain steel prices like hot-dipped galvanized steel, ultimately forced the index down. Experts anticipate this bearish pressure to continue impacting both steel prices and automotive manufacturing in the short term. Despite this, the automotive […]

EU Commission Reviews Request for 25% Extension of Steel Safeguard

The European Commission, the executive body of the European Union, is due to examine a request to extend a 25% safeguard on a range of steel imports. Steel news reports that the EC received a request from 14 member states of the 27-member bloc on January 12. This request aimed to establish if an extension of […]

Metinvest Reports Drop in Steel Production Amidst Russian Invasion

Ukrainian metals and mining group Metinvest recently reported a 31% decrease year on year in its crude steel production for 2023, citing Russia’s ongoing invasion of the country. The company halted steel manufacturing activities at its assets in Mariupol, Avdiivka, and Zaporizhzhia two years ago. This includes the Azovstal, Ilyich Steel, Avdiivka Coke, and Zaporizhzhia […]

UK Places Hot Rolled Steel Imports Under Scrutiny with Tata Steel Closure Plans

The United Kingdom’s Trade Remedies Authority (TRA) recently initiated a suspension review on safeguard measures against hot rolled flat and coil steels. Steel news sources report that the move also came alongside a tariff quota review. TRA reported on February 9 that both Tata Steel UK (TSUK) and steel trader Kromat Trading filed applications for […]

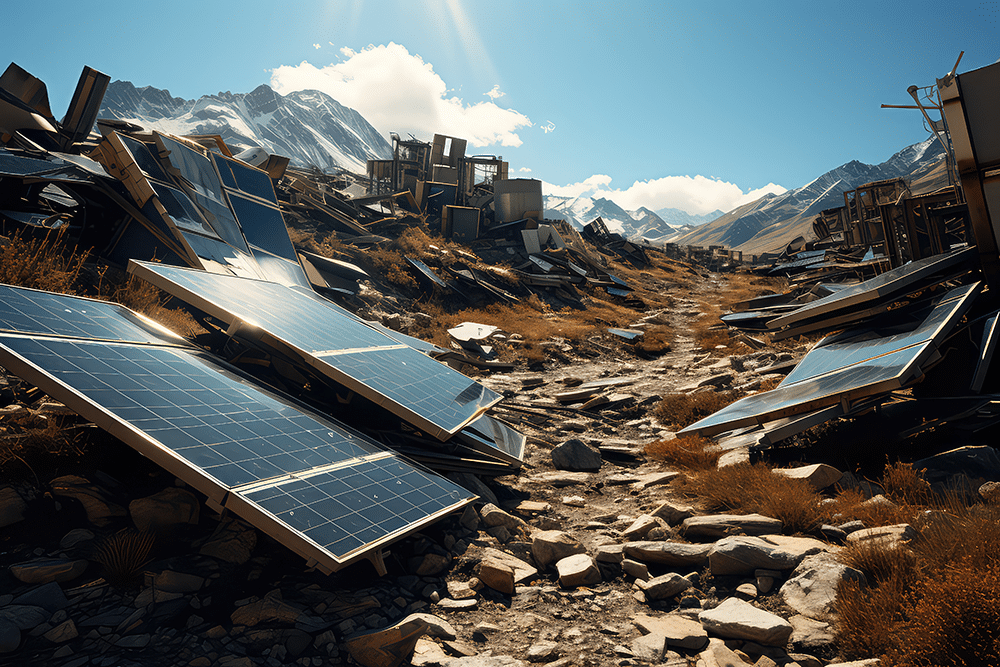

Renewables/GOES MMI: The “Dirty” Business of Disposing of Solar Panels

Numerous factors continue to pull at the Renewables MMI (Monthly Metals Index) as it moves through Q1. This past month, the index largely moved sideways, only exhibiting a slight upward movement of 1.66%. Meanwhile, renewable energy news indicated that metals like cobalt and silicon could remain in oversupply for some time. Moreover, expanding mining operations […]

Raw Steels MMI: Steel Prices Decrease as Nippon Deal Faces Setback

The Raw Steels Monthly Metals Index (MMI) fell 11.17% from January to February as steel prices declined. U.S. flat rolled steel prices continued to slide after finding a peak at the close of 2023. Following a 2% decline throughout January, hot rolled coil prices fell over 5% during the first half of February. HRC prices […]

Construction MMI: U.S. Construction Industry Enters 2024 Lacking Skilled Craftsman

The Construction MMI (Monthly Metals Index) moved in a relatively sideways trend, only budging up 0.65%. Steel prices continuing to flatten out, along with bar fuel surcharges dipping in price, kept the index from breaking out of the sideways movement we’ve witnessed since December. As the index enters 2024, U.S. construction news continues to focus […]