MetalMiner, the Leading Metal Intelligence Brand for Forecasting Metal Prices

When Metal Prices Become Volatile, How Do You Know When to Buy?

When steel prices shift due to trade policy changes, when 304 surcharges move higher due to rising nickel prices, or when copper rebounds due to a speculative rally, the question isn’t “What happened?” The correct question is “What should we do next?”

MetalMiner turns market disruptions and noise into a clearer, more actionable purchasing strategy, so you can evaluate the fairness of supplier quotes, negotiate with more leverage, and avoid overpaying.

Built on proprietary historical time series metal price data

Trusted MCP metal price provider across numerous sectors

Covering steel, stainless steel, aluminum, copper, critical minerals, and more

Why Do Metal Purchasing Decisions Become So Difficult?

Each metal type follows a different pricing structure.

Steel: Do extended lead times justify a higher mill price, or is the increase being made ahead of demand?

Stainless Steel: Is the price change coming from a specific part of the surcharge, or does it reflect a mill base price increase?

Copper: Is the move driven by physical demand or a short-term, speculative rally?

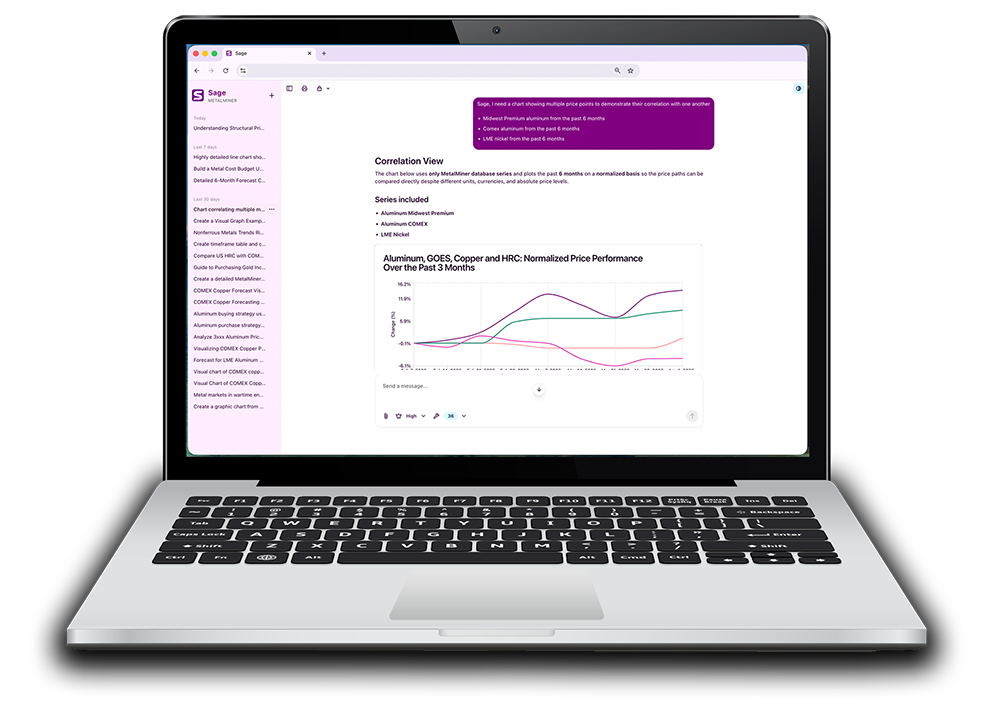

Meet Sage, MetalMiner's Category Manager

Sage is trained on nearly 6000 historical data sets and armed with 30+ metal-specific commodity tools. This helps organizations apply the right purchasing strategy at the right time by breaking down what is driving metal price volatility and what specific steps you should take next.

Most tools only show prices or a short-term forecast. Sage not only shows these things, but also explains how to respond to them.

What Does Sage Help Organizations Do?

It helps the buyer to determine exactly what sourcing strategy you should execute

It helps you understand what data you can use to counter a price increase during negotiations

Identify whether a price increase is tied to market benchmarks like the Midwest Premium or if the supplier is adding spread to the conversion premium

Separate market volatility from short-term futures, giving you knowledge about whether to purchase now or hold

Apply a consistent purchasing strategy

How Does Sage Work?

Sage empowers companies to connect market trends to accurate decision-making by focusing on the contents of each supplier quote.

Tracks the drivers behind each metal’s pricing, giving you stronger negotiation leverage

Breaks down what is driving the quoted price so teams know the fair price to pay

Recommends a clear purchasing response to save money and avoid lost revenue

Want to learn more about Sage to assist you with your metal sourcing strategies?

Applying highly specialized approaches to metal sourcing, based on metal type, market direction, and current market trends, instead of reacting quote by quote.

Strengthening Supplier Negotiations

Entering negotiations with a clearer understanding of what is driving prices and when to push back.

Reducing Overall Cost Risk

Avoiding lost revenue due to lack of clarity on current pricing drivers, poor timing, or supplier-led increases.

Achieving More Internal Alignment

Giving organizations a shared, structured view of pricing across metals markets.

Best Practice Library

What Are The Best Ways to Handle Metal Price Volatility?

Metal prices change fast, and supply chain surprises can throw off budgets and strain supplier relationships.

MetalMiner’s Best Practices Library gives companies a practical toolkit to handle it all. Learn real-world strategies to cut sourcing risks, protect your margins and stay ahead of costly market shifts.