From Noise to Action: How Leaders Turn Metal Market Signals into Supply Chain Decisions

Most organizations do not struggle to access metal prices or even price forecasts. They struggle to decide what those price movements should trigger across procurement, finance, and supply chain risk management.

Too often, markets are treated as background commentary. Procurement tracks prices, finance reacts to budget variance, and operations respond when suppliers reprice or lead times shift.

However, by then, the decision window has already passed.

A more effective approach reverses that sequence:

- Start with exposure mapping

- Define decision triggers

- Then act across sourcing, budgeting, contracts, inventory, and risk

This is where tools like Sage and MetalMiner’s category manager come in handy. Not because they provide more data, but because they help connect price movement to actual business exposure and decision timing.

The key shift is simple. Price movement is not insight. Actionable thresholds are.

What Does Price Movement Actually Tell You About Exposure and Supply Chain Risk Management?

A price chart is only useful when it reflects how your company buys, not just how the market moves.

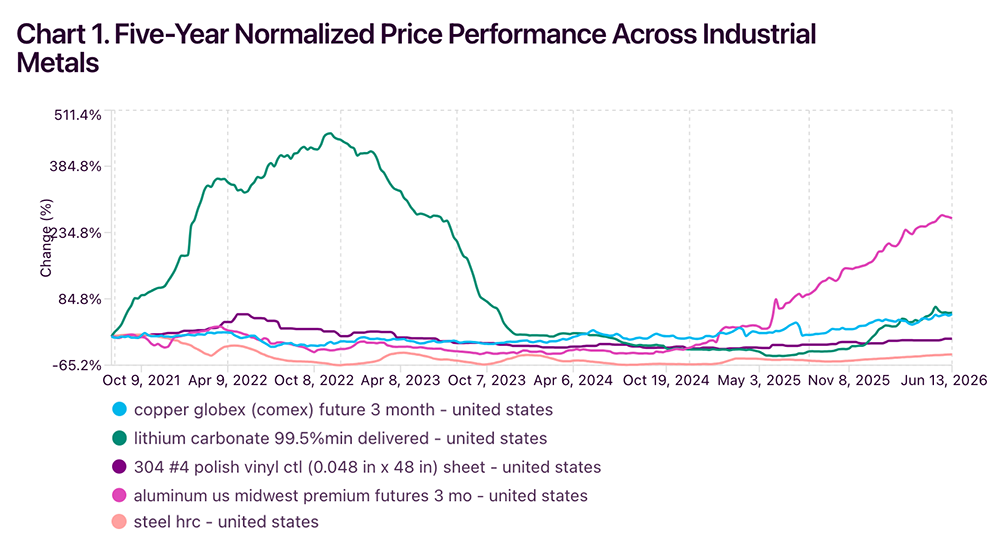

Very seldom do industrial metals move together. For instance, over the past 5 years:

- U.S. hot-rolled coil rose about 12.0%

- COMEX copper rose 83.9%

- U.S. 304 stainless sheet increased 19.8%

- U.S. Midwest Premium aluminum rose 796.2%

- Lithium carbonate increased 151.3% with extreme volatility

- Nickel ended only 3.2% higher despite major interim spikes

These differences are not just historical data. They directly affect budgeting, hedging, and supplier negotiations.

Correlation data reinforces the point:

- Hot-rolled coil vs aluminum: 0.019

- Hot-rolled coil vs copper: 0.237

There is no reliable “metals trend” you can apply across categories.

Procurement implication:

- You cannot budget steel using copper logic

- You cannot hedge stainless using nickel assumptions alone

- You cannot treat aluminum as a single risk factor

Exposure must be defined by what you actually buy, not what the market headline says.

How Should You Break Down Metal Cost Exposure?

The most important first step is decomposition. A single invoice price often hides multiple risks.

For example, a steel purchase may include:

- Base index exposure

- Contract lag

- Freight

- Supplier conversion costs

Aluminum makes this point even clearer:

- LME aluminum rose 69.1%

- U.S. Midwest Premium rose 796.2%

- Correlation: 0.763

- Shared variation: about 58.2%

That remaining gap is basis risk.

What this means for sourcing:

- Hedging the exchange does not neutralize total aluminum exposure

- Budgeting the premium as a minor line item creates hidden risk

- Ownership of each exposure component must be explicit

Better questions to ask:

- How much exposure sits in the base price vs the premium?

- Who owns each risk internally?

- Are we managing them separately or assuming they move together?

When Does a Market Signal Actually Matter?

A market signal matters when it forces a decision, not when it generates an opinion. The basics of this are all covered in The 5 Biggest Cost-Saving Sourcing Practices.

Support and resistance levels are useful because they define thresholds.

Current examples:

- Copper at $6.5355/lb sits just below resistance

- Hot-rolled coil near $1,101/st is already above long-term resistance

- Midwest Premium near $1.165/lb sits just above support

These are not predictions. They are decision triggers.

Operational questions they should prompt:

- Are open quotes still valid?

- Should budget assumptions be reviewed?

- Does contract language still protect us?

Standardized responses help teams act faster:

- Near resistance:

- Shorten quote validity

- Reopen supplier discussions

- Near support:

- Review staged buying plans

- Assess pre-approved coverage

What this means for finance:

- Test margin impact

- Revisit surcharge assumptions

What this means for supply chain leaders:

- Separate service inventory from price-driven inventory

How Do Contracts Turn Market Insight Into Savings?

Market awareness alone does not reduce costs. Contract structure does.

A historical example from MetalMiner’s buying strategy for hot-rolled coil shows:

- 4.08% cumulative savings vs spot

- Lower pricing on 462 days

- Higher pricing on 130 days

- Matched on 598 days

Large savings periods included:

- December 2023: 25.94%

- January 2024: 23.59%

- March 2025: 21.33%

- April 2025: 23.44%

The takeaway is not timing perfection. It is structured discipline.

Effective contracts:

- Separate committed and tactical volume

- Define reset windows

- Include re-opener clauses tied to market thresholds

What to avoid:

- Forcing all volume through one pricing mechanism

- Locking assumptions that cannot adjust to market shifts

What to do instead:

- Align contract design with observed price behavior

- Build flexibility where volatility is highest

Why Does Stainless Exposure Create Confusion for Finance?

Nickel is often used as a proxy for stainless. It should not be.

Data shows:

- Nickel vs 304 stainless correlation: 0.786

- Shared variance: about 61.7%

Over the same period:

- Stainless rose 19.8%

- Nickel rose only 3.2%

Nickel peaked sharply in March 2022. Stainless followed a different trajectory due to additional cost drivers:

- Chromium

- Scrap

- Conversion costs

- Mill pricing behavior

Procurement implication:

- A nickel hedge does not fully protect stainless exposure

Operating implication:

- Hedging decisions belong to risk management

- Purchase price outcomes depend on contract structure and surcharges

Key takeaway:

Separate the hedge conversation from the purchasing strategy. Treat them as related but distinct decisions. Learn these strategies in How Executive Teams Expect Procurement to Save Money.

How Should Inventory Strategy Reflect Market Conditions?

Inventory decisions often follow sentiment rather than policy.

That creates risk.

Volatility readings from 2021 to mid-2026 show:

- Stainless: 0.85

- Hot-rolled coil: 1.07

- Copper: 1.43

- LME aluminum: 1.22

- Midwest Premium: 2.06

- Nickel: 2.08

Along with this, lithium carbonate in particular showed extreme movement:

- Low near 6.77

- High around 79.33

- 11.7-fold range

What this means:

Not all inventory should be managed the same way.

Better segmentation:

- Service inventory for continuity

- Price-risk inventory for market positioning

Higher-volatility categories require:

- Tighter controls

- Shorter review cycles

- Clear approval thresholds

Without this separation, companies confuse:

- Working capital strategy

- Market speculation

How Do You Align Procurement, Finance, and Supply Chain Teams?

The biggest execution gap is not data. It is timing.

Most companies operate on separate clocks:

- Procurement follows supplier timelines

- Finance follows monthly close

- Operations follows plant urgency

This creates misalignment.

A better model uses a shared cadence:

- Daily:

- Monitor quote exposure

- Track support and resistance proximity

- Weekly:

- Review unpriced volume

- Assess supplier gaps

- Evaluate purchase timing

- Monthly:

- Reforecast budget exposure

- Validate contract assumptions

- Measure savings vs benchmarks

- Quarterly:

- Revisit strategy by metal category

This structure ensures:

- Decisions are synchronized

- Signals trigger coordinated action

- Exposure is managed proactively

Why This Matters

Metal markets do not damage margins because they move. They damage margins when companies fail to translate movement into action.

The real advantage comes from turning signals into:

- Defined thresholds

- Assigned owners

- Clear response timelines

What This Means for Your Sourcing Strategy

If there is one consistent pattern across metals, it is this:

Companies that outperform do not predict markets better. They respond to them more consistently.

Focus areas to strengthen:

- Decompose exposure by cost component

- Align contracts with price behavior

- Separate hedge strategy from purchasing decisions

- Segment inventory by purpose, not habit

- Establish shared decision cadence across teams

The goal is not to eliminate volatility. It is to manage it with structure.

Because with metal sourcing, the difference between noise and action is not the data. It is what the business is prepared to do when the signal appears.