Why Steel Price Forecasts Matter More Than Ever

Steel buying becomes much more difficult when price transparency disappears. For manufacturers, sourcing leaders, and finance executives, steel prices affect far more than purchase orders. They shape margins, customer quotes, inventory values, contract negotiations, and overall budget confidence.

That is why a disciplined approach to the development of steel price forecasts matters. The goal is not to predict the market with perfect precision. The goal is to improve how procurement teams interpret steel price trends, evaluate market structure, and make more informed sourcing decisions.

For MetalMiner, that means combining price history, technical analysis, statistical modeling, ML modeling into a framework buyers can actually use. Procurement teams need more than raw numbers. They need market context that helps explain what current pricing conditions mean for future buying decisions.

Why Do Steel Price Forecasts Matter?

Steel markets can move much faster than internal budgeting cycles. An annual budget may look reasonable when approved, only to come under pressure weeks later if mill prices rise, lead times extend, geopolitical tensions rise, or spot conditions tighten. That leaves procurement teams reacting instead of planning.

MetalMiner’s price data highlights why this matters. Over the last two years, U.S. hot-rolled coil rose from $806 per short ton to $1,055 per short ton, an increase of 30.9%.

More importantly, the market now sits at the top of its one-year range.

For executives managing cost exposure, that is not background noise. MetelMiner covers what executive teams expect from procurement teams more in-depth in How Executive Teams Expect Procurement to Save Money. What matters most is identifying clear signals that steel is already operating in a higher-cost risk zone.

As of the latest reading, hot-rolled coil sat about 3.9% above short-term support and 3.5% below short-term resistance.

That positioning matters because it signals to buyers that the expected trade band is operating within a narrow upper price band rather than in a relaxed or discounted environment.

Why Is Forecasting Steel Prices So Challenging?

Like most industrial metals, steel prices rarely move in a straight line.

Prices respond to shifts in demand, mill discipline, service center behavior, raw material pressure, and broader industrial sentiment. Procurement teams can usually see past price performance. However, the hard part is understanding what the market’s current position may signal next.

Averages do not tell buyers whether steel is consolidating, testing resistance, or breaking above prior trading levels. That is why a useful steel forecasting process needs more than backward-looking analysis. It needs market structure.

This is where support and resistance levels become commercially useful.

Support highlights zones where buying interest has historically emerged. Resistance highlights areas where prices have struggled to move higher. In procurement terms, those are not abstract technical indicators. They are practical reference points that can support:

- Contract timing decisions

- Inventory planning

- Budget forecasting

- Internal approvals

How Does MetalMiner Help Buyers Interpret Steel Price Direction?

MetalMiner’s role is not to reduce the steel market to a single headline number.

The goal is to help buyers build a defensible market view using multiple forms of evidence. That includes:

- Historical price trends

- Technical support and resistance levels

- Price volatility

- Spreads

- Category-specific market intelligence

- Cross-market analysis across industrial metals

- Disruption modeling to understand how black swan events will impact pricing

MetalMiner’s market coverage extends across steel, stainless, aluminum, copper, and critical minerals. That matters because procurement decisions rarely happen in isolation.

A sourcing team managing steel sourcing risks often has cost exposure to adjacent inputs as well. Better decision-making comes from understanding whether steel is moving independently or whether broader industrial metals are reinforcing the same cost pressure.

What Does Broader Metals Strength Mean for Steel Buyers?

Steel does not move in isolation.

Over the last two years:

- U.S. hot-rolled coil gained 30.9%

- COMEX copper rose 34.3%

- LME aluminum increased 38.7%

MetalMiner data from Sage also shows a strong positive correlation between steel and copper over that period of 0.84, along with a solid positive relationship between steel and aluminum of 0.69.

That broader pattern matters for executive teams.

If steel, copper, and aluminum are all trading near the upper end of their annual ranges, the issue is no longer isolated to one category. It becomes a wider procurement cost issue that affects budgeting, quoting, and margin planning across multiple inputs.

This type of multi-metal visibility improves procurement planning by allowing sourcing and finance teams to think in terms of portfolio exposure rather than isolated commodities.

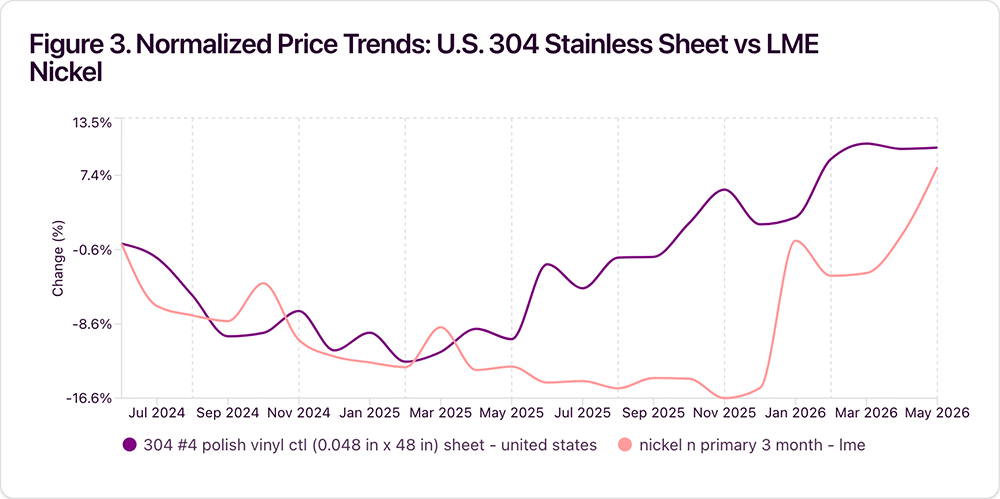

What Can Stainless and Critical Minerals Teach Buyers About Forecasting?

One of the biggest forecasting mistakes procurement teams make is assuming one metal fully explains another.

Stainless steel offers a good example.

Over the last two years, U.S. 304 stainless steel sheet increased 10.3%, while LME nickel rose only 1.7%. The monthly correlation between the two was 0.49, which is something, but far from complete.

Nickel matters, but it does not explain the full stainless steel cost picture.

That is an important lesson for procurement organizations. Shorthand assumptions often create blind spots. Stainless requires stainless-specific analysis, just as steel requires steel-specific analysis.

The same logic applies to critical minerals.

MetalMiner data shows lithium carbonate delivered pricing moving from approximately $15.25 per kilogram to $20.44 per kilogram over the last two years, with a period low of roughly $7.33 per kilogram.

That kind of range reinforces why procurement teams increasingly need a cross-category approach to price risk management.

What This Means for Your Sourcing Strategy

Procurement teams do not need certainty to improve decision-making. They need better visibility into market conditions, trading ranges, and potential cost exposure.

That changes how organizations approach:

- Budget planning: Evidence-based pricing ranges are more useful than static data.

- Contract timing: Technical positioning can help buyers evaluate whether prices are testing support, approaching resistance, or operating in elevated territory.

- Inventory strategy: Understanding broader pressure in metal markets helps teams evaluate whether conditions are isolated or systemic.

- Internal communication: Procurement leaders can better explain not only what they purchased, but why they purchased it when they did.

Why Does Scenario-Based Planning Matter?

Forecasting becomes more practical when it connects directly to real-time risk scenarios.

Procurement leaders do not just need a view of historical price behavior. They need a framework for evaluating why prices change when external conditions change.

That is why scenario-based planning plays such an important role in modern price risk management.

MetalMiner’s steel market intelligence helps buyers assess how changes in trade conditions or broader disruptions in the metals sector could affect purchasing conditions. Even when the goal is not to publish a precise directional call, scenario analysis still improves decision-making.

It helps procurement teams:

- Test assumptions

- Evaluate exposure

- Ask better sourcing questions

- Prepare for changing market conditions before cost pressure reaches the budget

Why Better Visibility Leads to Better Steel Decisions

The question is not whether companies can predict the future with certainty, but rather if procurement teams can build a more disciplined and more confident view of the steel market using reliable evidence.

That is what a useful steel price forecast should provide.

MetalMiner helps buyers do that by combining steel price trends, support and resistance analysis, broader steel market conditions, and scenario-based planning into one market intelligence framework.

For companies managing exposure across steel, copper, aluminum, stainless, and critical minerals, that visibility supports:

- Smarter budgeting

- More informed sourcing decisions

- Better contract timing discussions

- Stronger risk management discipline

- Improved procurement planning in volatile markets

In uncertain metal environments, better visibility leads to more revenue.