Construction MMI: Bar Fuel Surcharges Drop, Steel Prices Edge Up

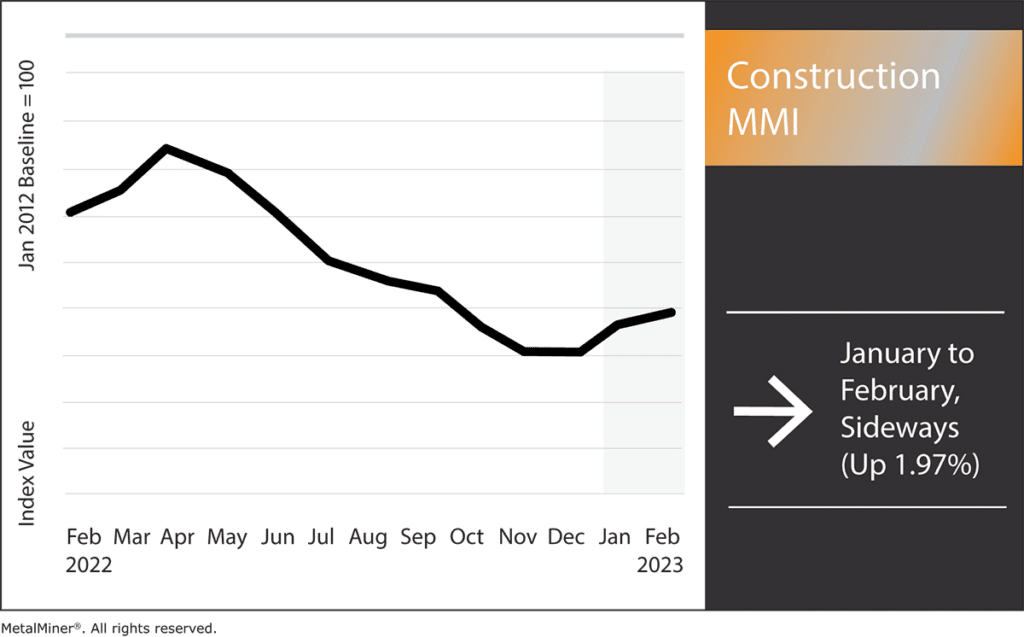

The Construction MMI (Monthly MetalMiner Index) traded sideways, rising by just 1.97%. The index was pulled in multiple directions month-over-month, resulting in a lack of major movements. For instance, bar fuel surcharges dropped, while steel rebar, h-beam steel, and sheet aluminum all went up. This recent rise in steel prices has left the index facing bullish pressure.

Most metal components of the construction index rose in price last month. Steel rebar, in particular, felt the impact of a slower-than-anticipated Chinese recovery after the country lifted its zero-COVID restrictions. The same remains true for h-beam steel. Meanwhile, European aluminum commercial 1050 sheets jumped in price significantly. Due to high energy costs, many European aluminum producers are still operating at limited capacity.

Buy metal with confidence. MetalMiner Insights offers in-depth purchasing advice, price comparison tools, forecasts and comprehensive should-cost models. Click to schedule a demo.

Where are Construction Prices Going? The Impact of Steel Prices…

Construction costs turned upward in January, leaving experts wondering if even higher costs are on the horizon. While softening mortgage rates left builders feeling optimistic, the industry still faces significant challenges. Two major hurdles are the slow recovery of China in the wake of zero-COVID and rising steel prices.

Fortunately, labor is slowly returning to the industry. In fact, U.S. construction firms added 25,000 new employees in January. This comes as a huge relief after 2022, when the market struggled with constant labor shortages. Additionally, the average pay within the construction industry began increasing in January, providing an extra incentive to potential applicants. So, at least for the labor end of construction, the year has started out promising.

Despite this, material costs are now climbing, particularly Chinese-sourced steel. In the short term, any Chinese-sourced construction steel forms like h-beam steel and steel rebar will likely trend upward. Another thing to note is the current state of the iron ore market. A vital raw material for all steel production, iron faces significant supply constraints due to winter weather in China and Brazil. Therefore, buyers should remain wary, as this could impact the steel material market further.

MetalMiner’s weekly newsletter provides updates on shifting steel prices and market trends, as well as other commodity news. Sign up here.

Infrastructure Funding Could Increase

The U.S. House of Representatives has new legislation that would form a bank to invest in U.S. infrastructure. This would not only lead to more jobs in the construction industry but also greatly aid aging infrastructure across the country. If passed, the bipartisan Federal Infrastructure Bank Act of 2023 would create a sector that would work with state and local officials to match infrastructure projects with loans and loan guarantees.

The act could potentially raise the demand for construction materials like steel rebar and aluminum commercial 1050 sheet. This means that energy grids, and by extension, metal products like grain-oriented electrical steel, would see increased demand as well.

Unfortunately, there may be downsides. For instance, the act would require all steel and other construction materials to be manufactured within the U.S. This is great in terms of stimulating the U.S. industrial and jobs markets. However, it also means that vital construction materials like steel rebar wouldn’t be easy to obtain for qualifying projects. The steel rebar used in the U.S. primarily comes from China, Turkey, Algeria, and Mexico. That said, no doubt U.S. steel rebar manufacturers like Nucor and Admiral Steel would likely enjoy an influx in business.

By calling a bullish market or calling a bearish market, buying organizations can always generate cost savings or cost avoidance. Read MetalMiner’s track record.

Construction MMI: Notable Price Trends

- Chinese h-beam steel rose by 7.38%, setting prices at $588.42 per metric ton.

- The Weekly Midwest bar fuel surcharges decreased by 16.67%, leaving prices at $0.65 per mile.

- Chinese steel rebar increased in price by 4.41%, bringing them to $638.06 per metric ton.

- Finally, European commercial 1050 aluminum sheet rose by 5.05%, leaving prices at $4,155.53 per metric ton.

Leave a Reply