The Stainless Steel Monthly Metals Index (MMI) skyrocketed this month, increasing by seven points. The current reading stands at 84. Need buying strategies for steel? Try two free months of MetalMiner’s Outlook The index inched higher driven by the increase in stainless steel surcharges and a sharp increase in LME nickel prices in May. Other […]

Tag: stainless steel price

Stainless Steel MMI: Subindex Inches Upward on Rising LME Nickel Prices

In May, the Stainless Steel Monthly Metals Index (MMI) once again inched one point higher. The current reading stands at 77 points. Need buying strategies for steel? Try two free months of MetalMiner’s Outlook The subindex inched higher driven by increasing LME nickel prices. Meanwhile, other related metals in the stainless steel basket traded flat. […]

Stainless Steel MMI: LME Nickel Prices Fall But Stainless Steel Surcharges Rise

The Stainless Steel MMI (Monthly Metals Index) inched one point higher in April. The current reading is 76 points.

Need buying strategies for steel? Try two free months of MetalMiner’s Outlook

The index’s increase was driven by the rise in stainless steel surcharges, despite slightly falling LME nickel prices this month. Other related metals in the stainless steel basket increased.

LME Nickel

In April, nickel price momentum appears to have recovered from its previous pace.

LME nickel prices dropped in March, along with other base metals. However, the drop appears less sharp than for aluminum or copper.

[caption id="attachment_91260" align="aligncenter" width="580"] Source: MetalMiner analysis of FastMarkets[/caption]

Source: MetalMiner analysis of FastMarkets[/caption]

LME nickel prices remain high and far away from 2017 lows back in May or June, when MetalMiner recommended buying organizations buy some volume forward. Prices back at that time were around $8,800/mt versus the current $13,200/mt price level.

Domestic Stainless Steel Market

Following the recovery in stainless steel momentum, domestic stainless steel surcharges increased this month.

The 316/316L-coil NAS surcharge reached $0.96/pound. Therefore, buying organizations may want to look at surcharges to identify opportunities to reduce price risk either via forward buys or hedging.

[caption id="attachment_91261" align="aligncenter" width="580"] Source: Source: MetalMiner data from MetalMiner IndX(™)[/caption]

Source: Source: MetalMiner data from MetalMiner IndX(™)[/caption]

The pace of stainless steel surcharge increases appears to have slowed this month. However, surcharges have increased from 2017. The 316/316L-coil NAS surcharge is closer to $0.96/pound.

What This Means for Industrial Buyers

Stainless steel momentum appears stronger this month, with steel prices skyrocketing.

As both steel and nickel remain in a bull market, buying organizations may want to follow the market closely for opportunities to buy on the dips.

To understand how to adapt buying strategies to your specific needs on a monthly basis, take a free trial of our Monthly Outlook now.

MetalMiner’s Annual Outlook provides 2018 buying strategies for carbon steel

Actual Stainless Steel Prices and Trends

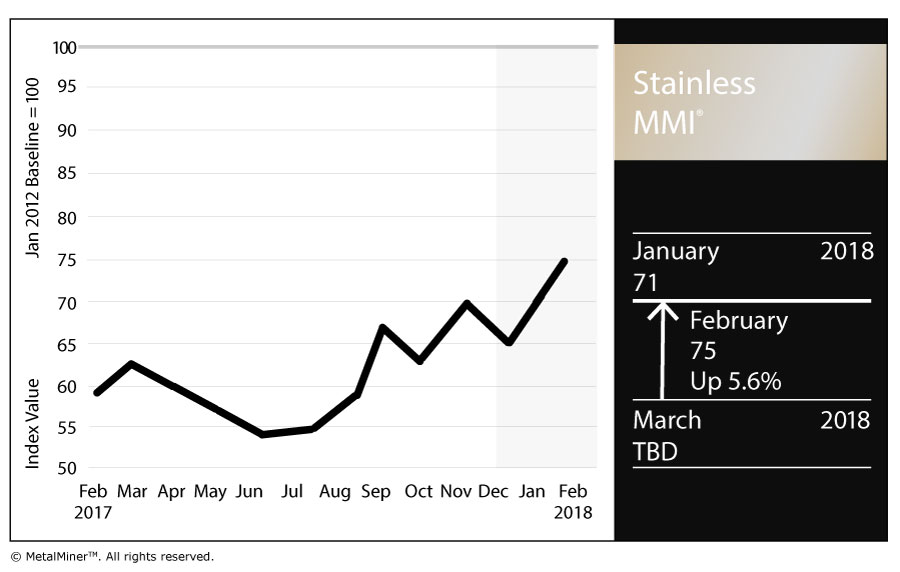

Stainless Steel MMI: LME Nickel Price, Stainless Surcharges Both Rise

The Stainless Steel MMI (Monthly Metals Index) jumped four points again this month for a February reading of 75.

Need buying strategies for steel? Try two free months of MetalMiner’s Outlook

In January, skyrocketing LME nickel prices drove the Stainless Steel MMI. Nickel prices have climbed above the $13,000/mt level. 304 and 316 surcharges increased this month, returning to their previous levels.

LME Nickel

Nickel prices increased sharply during January. However, prices decreased slightly in early February. As reported previously by MetalMiner, nickel price volatility has increased over the past few months. Therefore, nickel prices may prove quite tumultuous from a short-term perspective and are trading within the orange-dotted band in the chart below.

[caption id="attachment_90272" align="aligncenter" width="580"] Source: MetalMiner analysis of FastMarkets[/caption]

Source: MetalMiner analysis of FastMarkets[/caption]

The long-term nickel price uptrend also remains strong. Prices have moved toward June 2015 levels and already breached our October 2017 long-term resistance levels, as per our Annual Outlook. Therefore, nickel prices remain in a strong uptrend and could continue increasing in the coming months.

Domestic Stainless Steel Market

Following the recovery in stainless steel momentum, domestic stainless steel surcharges increased this month. Surcharges remain above last year’s lows (under $0.4/pound); they remain in an uptrend, even if their pace has slowed. However, buying organizations may want to look at surcharges closely to reduce risks, either via forward buys or hedging.

[caption id="attachment_90273" align="aligncenter" width="580"] Source: MetalMiner data from MetalMiner IndX(™)[/caption]

Source: MetalMiner data from MetalMiner IndX(™)[/caption]

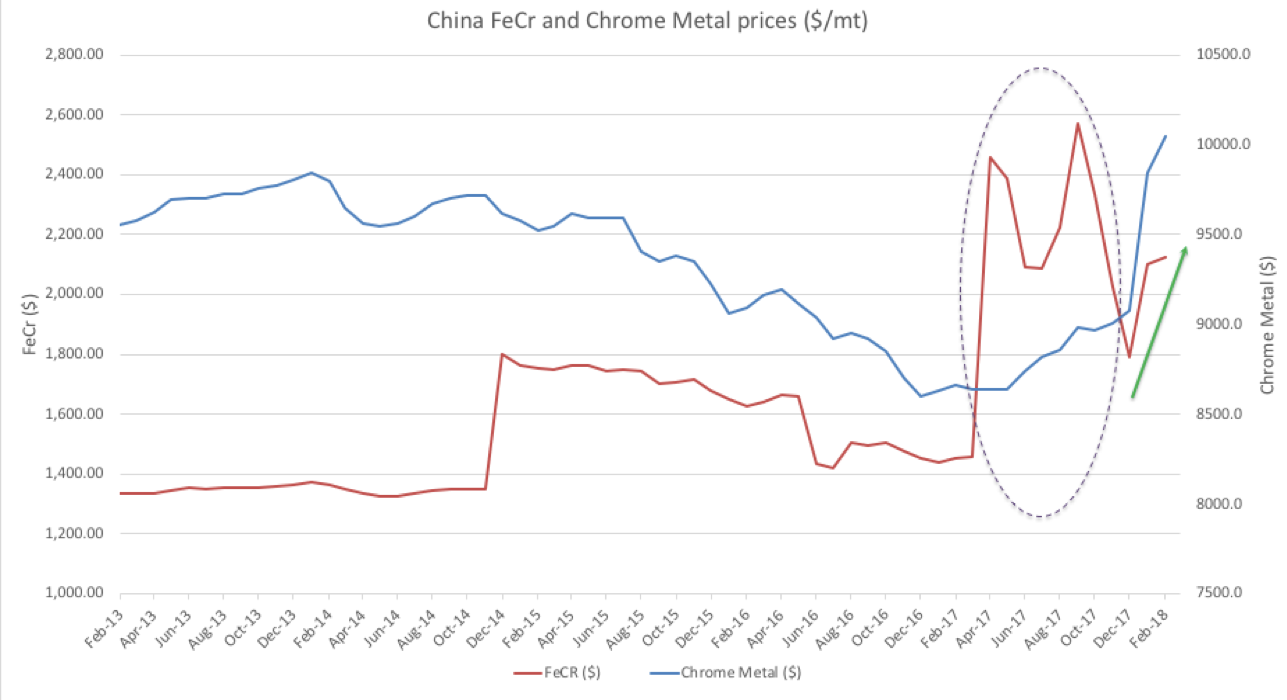

FerroChrome vs. Chrome Metal

Two months ago, MetalMiner reported on the anomaly between ferrochrome and chrome metal prices.

[caption id="attachment_90274" align="aligncenter" width="580"] Source: MetalMiner data from MetalMiner IndX(™)[/caption]

Source: MetalMiner data from MetalMiner IndX(™)[/caption]

Ferrochrome (FeCr) is a chromium and iron alloy containing 50% to 70% chromium by weight. Historically, Ferrochrome and chrome prices correlate tightly but the high iron ore prices caused ferrochrome to spike. However, both prices (ferrochrome and chrome) have fallen back to their historical trading pattern of moving together.

What This Means for Industrial Buyers

Stainless steel momentum appears in recovery, similar to all the other forms of steel. As both steel and nickel remain in a bull market, buying organizations may want to follow the market closely for opportunities to buy on the dips. To understand how to adapt buying strategies to your specific needs on a monthly basis, take a free trial of our Monthly Outlook now.

MetalMiner’s Annual Outlook provides 2018 buying strategies for carbon steel

Actual Stainless Steel Prices and Trends