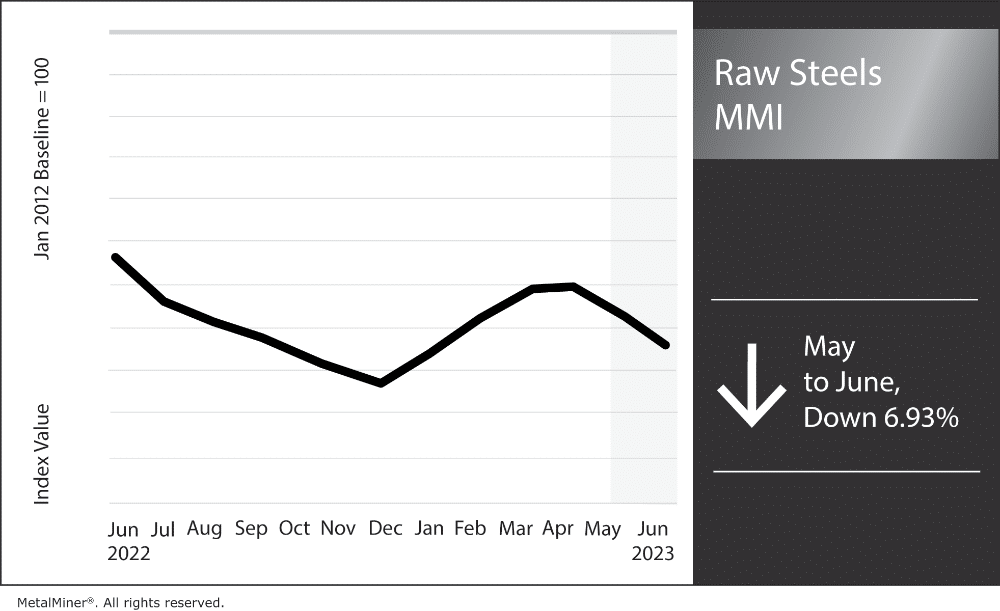

Raw Steels MMI: HRC Steel Prices Drop and Mill Lead Times Plummet

The Raw Steels Monthly Metals Index (MMI) remains bearish, declining 6.93% from May to June. Flat rolled steel prices returned to their bearish movement after peaking in April, while hot rolled coil prices retraced down to their March levels. Altogether, HRC prices have declined 13% from their April 14 high. Meanwhile, both cold rolled coil and hot dipped galvanized prices saw an even sharper month-over-month decline, while plate prices returned sideways, sliding less than 1%.

MetalMiner’s free weekly newsletter provides up-to-date metal price intelligence.

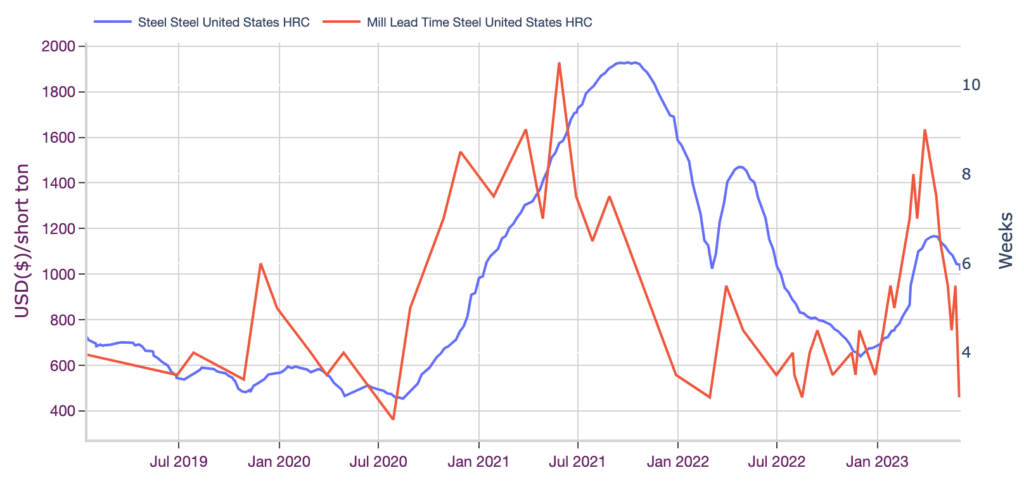

Average Mill Lead Times Drop to August 2022 Lows

As U.S. flat rolled steel prices inverted to the downside, average mill lead times dropped to their lowest levels in more than a year. Meanwhile, HRC mill lead times averaged three weeks at the close of May. This is their lowest production time since August 2022, and only slightly longer than their all-time low (since MetalMiner began tracking lead times in December 2018) of 2.5 weeks in July 2020.

While prices and mill lead times have a low overall correlation, mill lead times tend to shift ahead of price trend reversals. This continues to make lead times a relevant leading indicator for prices. Mill lead times first began to retrace back in April after they peaked at nine weeks near the end of March. This is roughly two weeks ahead of the HRC price peak. Except for a short-lived rise toward the end of May, lead times became increasingly shorter throughout the month.

Are you under pressure to generate steel cost savings? Make sure you are following these five best practices.

Market Backwardation, Lower Imports Indicate Bearish Market

Despite falling prices and shorter mill lead times, some reports indicate skepticism among certain mills and service centers. Argus Media reported that healthy shipments throughout May led some sellers to question the currently bearish price direction. Some speculated that the declines were largely due to buyer hesitancy rather than a meaningful erosion of end-use demand. While the economic outlook continues to worsen and the cost of holding onto inventories remains high, markets appear to see things differently, as spot and future prices remain in backwardation.

At the close of May, HRC spot prices sat at a $250/st premium over Midwest future prices. While this delta contracted slightly from the almost $300/st spread earlier in the month, it nonetheless reflects ongoing bearish sentiment among market participants. Since 2011, spot prices have carried an average $23/st premium over future prices. This figure is considerably lower than the current spread.

Meanwhile, imports began to slide as well. According to preliminary data from the U.S. Census Bureau, HRC imports during April saw a 12.83% decrease from March, and license data from the U.S. Department of Commerce suggests imports continued to decline during May. On top of falling prices and shorter mill lead times, a decline in imports appears emblematic of a falling demand market.

Discover what else impacts the U.S. steel market and generate hard savings on your metal buys year-round. Trial MetalMiner’s monthly outlook report.

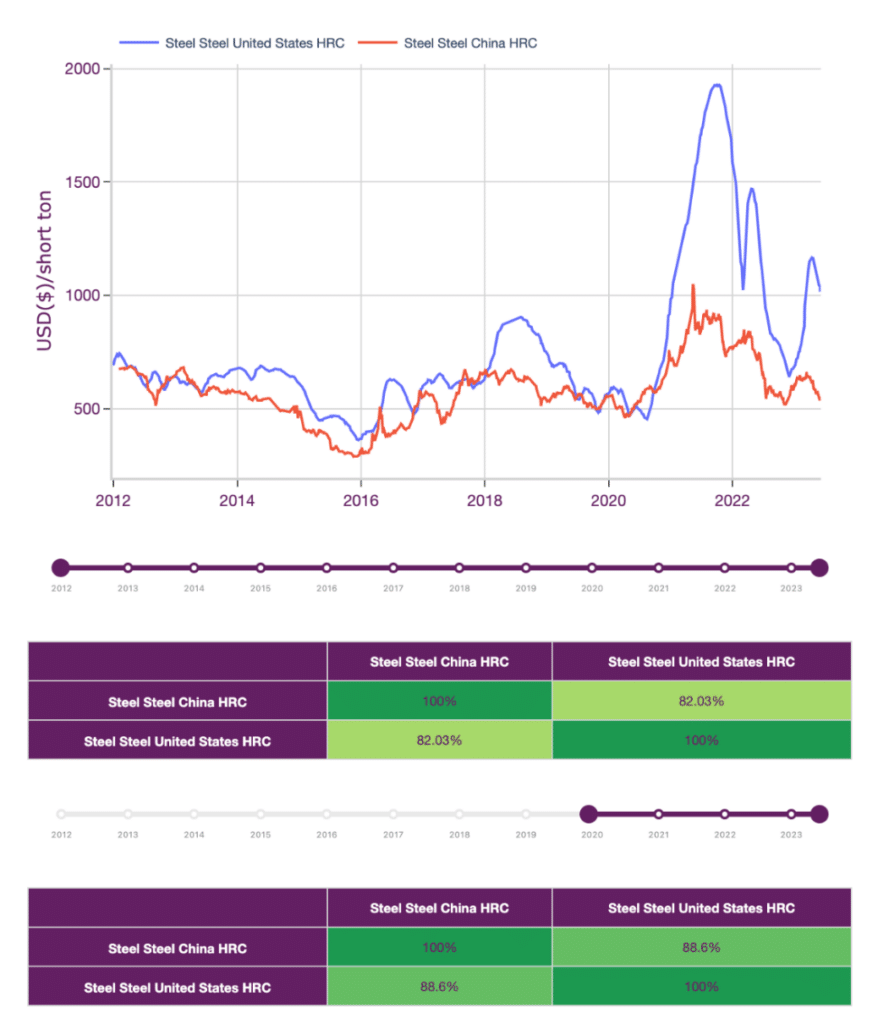

China Steel Prices Weak Amid Stimulus Moves

Worldwide, Chinese steel prices also remain weak. This is contrary to market expectations ahead of the country’s return from zero-COVID. Chinese steel prices historically represent the global bottom. However, starting in 2012, Chinese HRC prices began boasting an 82% correlation with U.S. prices. That correlation appeared to strengthen in recent years, rising to almost 89% from 2020 onward.

Falling Chinese steel prices appear indicative of a largely bearish global market. China’s ongoing recovery has largely benefited its service sector rather than industrial metals, as occurred in past recoveries. While China has not resumed any of its harsh control policies, a new wave of COVID expected to peak at the end of June will likely temper already-muted consumer demand.

China’s manufacturing sector did manage to return to growth last month. Still, the overall weakness within the Chinese economy has led to new expected stimulus measures that could add support to steel prices. On June 2, China’s cabinet, the State Council, announced a targeted package that would extend tax exemptions for EV purchases. Reports also suggest officials may initiate tax breaks for high-end manufacturers and provide additional support for the property market. Such stimulus hopes helped Chinese coking coal and iron ore prices find a bottom in late May.

CRU is a popular steel contracting index. But you shouldn’t use it very often. See why!

Biggest Moves for Raw Materials and Steel Prices

- Midwest HRC future prices fell 6.6% to $792 per short ton as of June 1.

- U.S. shredded scrap prices saw a 6.79% decline to $467 per metric ton.

- Chinese steel slab prices dropped by 7.77% to $601 per metric ton.

- Chinese HRC prices fell 8.16% to $552 per short ton.

- Finally, Chinese coking coal prices saw the largest month-over-month decline of the index for the second consecutive month, with a 15.7% drop to $267 per metric ton.

Leave a Reply