Chinese automaker BYD recently appointed Austria’s Voestalpine as its first steel supplier for the planned production plant in Hungary. On June 24, the Linz-headquartered steel industry leader officially announced it will begin supplying autobody and outer-skin components from its rolling mills to BYD’s Szeged plant in Q4 2025. Szeged sits about 180 kilometers south of […]

Christopher Rivituso

Steel Giant Bows Out: Who’s Taking Over Bosnia’s Mills?

ArcelorMittal recently announced the sale of its steel plant as well as its stake in its iron ore mine in Bosnia and Herzegovina, with news reporting stating that the steel industry giant will unload the plant to Bosnian industrial conglomerate Pavgord Group. According to the details of the deal, Pavgord Group will acquire the longs […]

Can a $673M Railway Deal Keep British Steel on “Track?”

British Steel has secured a 5-year agreement to supply rail to Network Rail, the infrastructure manager of the UK’s rail network. Under the tenets of the deal, the steelmaker will provide 70,000 to 80,000 metric tons per year. In a June 17 statement, British Steel reported that the contract is worth £500 million (almost $673 […]

Steel Titans: Who’s Up and Who’s ‘Melting Down’?

According to the World Steel Association (worldsteel), one of the leading providers of steel market information, the China Baowu Group was the largest steelmaker group in 2024, with production remaining stable on the year. In its June 5 report, titled “2025 World Steel in Figures,” worldsteel stated that the Shanghai-headquartered company poured just over 130 […]

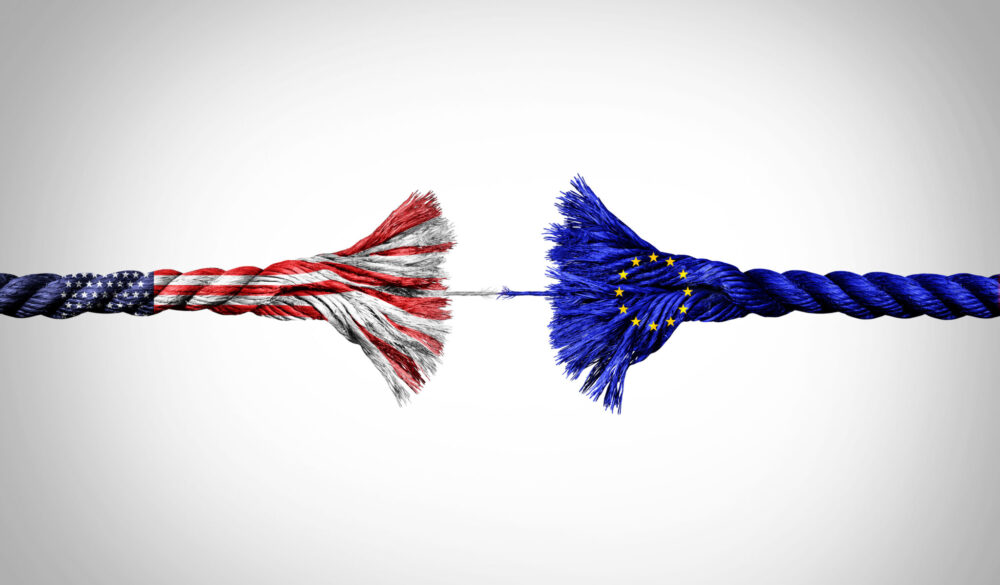

Steel Showdown: EU Warns Retaliation as Trump Doubles Down on Tariffs

The European Commission (EC) has expressed concern about Donald Trump’s announcement of plans to double import tariffs on steel. The U.S. President proclaimed the new “Trump Tariffs” during a speech at US Steel’s Mon Valley-Irwin works in Pennsylvania on May 30. “We strongly regret the announced increase of U.S. tariffs on steel imports from 25% […]

Tariff Ticking Time Bomb: Trump Gives UK Until July 9th to Avoid Steel Shock

Trump tariffs are back once again putting U.S trade partners in a tough spot. President Donald Trump recently exempted the United Kingdom from his doubling of import tariffs on steel and aluminum into the United States, but only temporarily. While import tariffs from UK steelmakers remain at 25% for now, failure to reach an agreement […]

Is Volvo’s Restructuring a Warning Signal for Steel Demand?

In late April, Swedish automaker Volvo announced plans to cut up to 3,000 jobs, or about 15% of its workforce, as part of a restructuring plan. Since then, steel industry insiders have pointed to the event as a potential warning sign for demand. According to statements from Volvo Cars CEO Håkan Samuelsson released on May […]

Auto Shock: Trump’s 25% Tariff Sends Europe Reeling

The “Trump Tariffs” continue to shock global markets, affecting multiple major sectors. Recently, European auto manufacturing ombudsmen reacted with alarm to President Donald Trump’s imposition of a 25% import tariff on auto imports into the United States. EU Auto Leaders React to Trump Tariffs Hildegard Müller, president of the German Association of the Automotive Industry, […]

Did the UK Take a Steel Giant Hostage to Save Its Industry?

The UK Parliament recently passed a law allowing the government to take control of British Steel, a major player in the local steel industry. The move follows Chinese owner Jingye’s plans to shut down two operating blast furnaces at its Scunthorpe site. A Bold Move Towards UK Steel Industry Preservation The House of Commons, Parliament’s […]

Tata Steel Ups its Game at Port Talbot With $1.56B Overhaul

Tata Steel recently signed an agreement to install a new pickling line at its Port Talbot site in Wales. The steel industry leader’s latest move will offer 50% more capacity than the existing line. According to the company’s April 9 announcement, the new equipment will have an annual capacity of 1.8 million metric tons and […]