The Automotive MMI (Monthly Metals Index) moved sideways, rising a slight 1.39%. As a whole, the US automotive market is facing a number of challenges necessitating both innovation and resilience. Why Are Critical EV Minerals in Short Supply? Automakers are grappling with shortages of critical minerals needed for electric vehicles and high-tech components. Rare earth minerals […]

Category: Automotive

Will a 15% U.S. Tariff on EU Autos Reshape Global Car Trade?

In a move with major implications for the global automotive industry, the U.S. federal government has implemented a 15% import tariff on auto imports from the European Union. According to a federal register notice from September 24, the move affects cars as well as auto parts. That notice went on to indicate that the duties […]

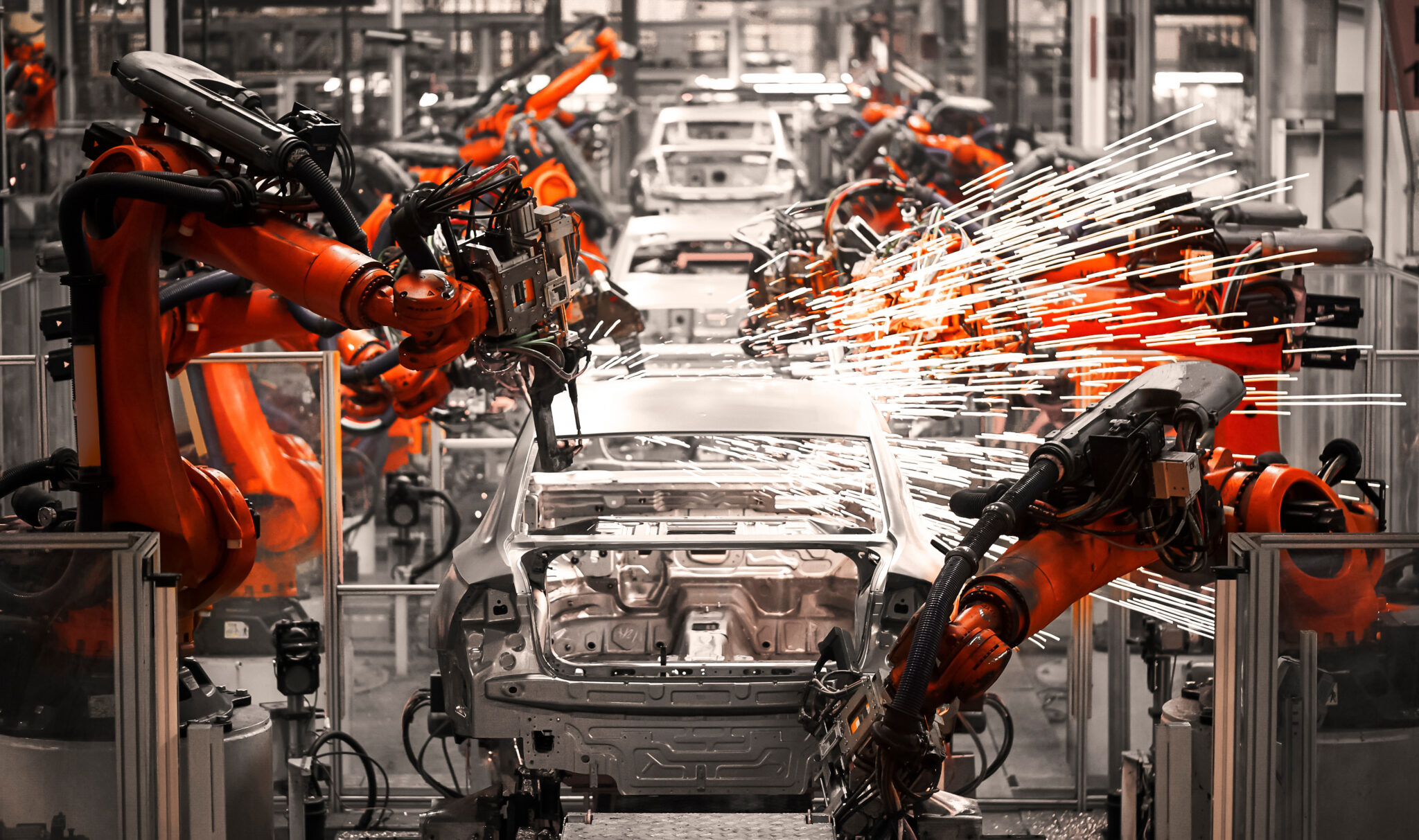

Automotive MMI: U.S. Automakers Grapple with Metal Supply Complications

The Automotive MMI (Monthly Metals Index) moved sideways, dropping a slight 2.3%. This comes as the US automotive market, manufacturers in particular, are facing a one-two punch of rising costs and potential shortages in their metal supply chains. A big reason for this is steep tariffs on steel, aluminum and other inputs, which are driving […]

Automotive MMI: Tariffs Fuel Turbulence in Auto Metals, U.S. Automakers Face Summer Price Spikes

The Automotive MMI (Monthly Metals Index) moved sideways, dropping by 0.84%. The U.S. automotive sector is reeling from recent developments that are dramatically altering the landscape for metal sourcing and procurement. Over the past month, new metal tariffs and trade deals, wild swings in aluminum and copper prices and frank warnings from automakers have converged […]

Automotive MMI: Automakers Scramble as Rare Earths Crunch and Tariffs Impact Supply Chains

The Automotive MMI (Monthly Metals Index) moved sideways month-over-month, dropping by 0.70%. This comes as auto industry executives in the U.S. are confronting a whirlwind of trade and supply chain disruptions, not to mention the effects of the recent round of Trump tariffs. In the past month alone, high-stakes U.S.–China trade talks, critical mineral export […]

Is Volvo’s Restructuring a Warning Signal for Steel Demand?

In late April, Swedish automaker Volvo announced plans to cut up to 3,000 jobs, or about 15% of its workforce, as part of a restructuring plan. Since then, steel industry insiders have pointed to the event as a potential warning sign for demand. According to statements from Volvo Cars CEO Håkan Samuelsson released on May […]

Automotive MMI: Volatile Steel and Copper Prices Shake U.S. Auto Industry

The Automotive MMI (Monthly Metals Index) moved sideways this past month, dropping a slight 1.74%. The US automotive industry faces a bumpy ride as key metal prices continue to swing wildly. In recent weeks, critical inputs like hot-dipped galvanized steel, copper and lead have seen rapid price shifts amid new tariffs and supply chain jitters, […]

How U.S. Manufacturers Shift Gears and Save Money Amid Metal Price Volatility

U.S. manufacturers in the automotive, appliance and general industrial sectors are overhauling procurement strategies as economic volatility and swings in steel, aluminum and copper prices squeeze margins. Recent U.S. tariff actions have jolted metals markets, sending input costs soaring for downstream manufacturers. According to Reuters, the uncertainty not only triggered panic buying but extended lead times […]

Automotive MMI: New 25% Automotive Tariffs in Effect, How is the Market Responding?

The Automotive MMI (Monthly Metals Index) rose by 4.33% month-over-month. With the 25% Trump tariffs now in effect, the market could be in for a bumpy ride. New Wave of Trump Tariffs Hit The Trump Administration implemented two sweeping trade actions, collectively known as the “Trump Tariffs,” that are reverberating across U.S. industries. First came […]

Automotive MMI: Hot-Dipped Galvanized Prices Spike Amongst New Tariffs

The Automotive MMI (Monthly Metals Index) increased by 4.47% month over month. The primary culprit for the bullish sentiment was hot-dipped galvanized prices rising due to tariff anticipation from the automotive industry. U.S. Automotive Industry Faces Rising Costs and Trade Challenges The U.S. automotive sector is grappling with economic pressures that could alter its operational […]