This morning in metals news, JFE Holdings Inc. in Japan plans to spend $6 billion on upgrades in the coming years, the Congressional Steel Caucus asked the administration for guidance on the Section 232 action timeline and Shanghai copper posted its biggest price jump since October. Need buying strategies for steel? Try two free months […]

Category: Metal Prices

This Morning in Metals: Metal Firms Line Up to Bid for Distressed Essar Steel

This morning in metals, several companies are looking to buy the distressed Essar Steel India Ltd., copper prices bounced back up and gold prices are up. Need buying strategies for steel? Try two free months of MetalMiner’s Outlook Essar Steel on the Market Companies like ArcelorMittal and VTB Group are vying for embattled Indian firm […]

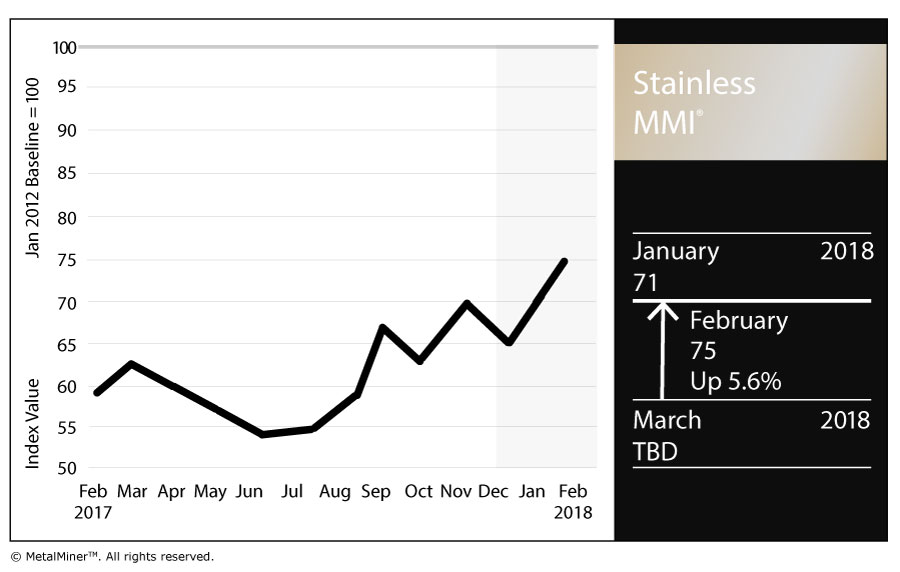

Stainless Steel MMI: LME Nickel Price, Stainless Surcharges Both Rise

The Stainless Steel MMI (Monthly Metals Index) jumped four points again this month for a February reading of 75.

Need buying strategies for steel? Try two free months of MetalMiner’s Outlook

In January, skyrocketing LME nickel prices drove the Stainless Steel MMI. Nickel prices have climbed above the $13,000/mt level. 304 and 316 surcharges increased this month, returning to their previous levels.

LME Nickel

Nickel prices increased sharply during January. However, prices decreased slightly in early February. As reported previously by MetalMiner, nickel price volatility has increased over the past few months. Therefore, nickel prices may prove quite tumultuous from a short-term perspective and are trading within the orange-dotted band in the chart below.

[caption id="attachment_90272" align="aligncenter" width="580"] Source: MetalMiner analysis of FastMarkets[/caption]

Source: MetalMiner analysis of FastMarkets[/caption]

The long-term nickel price uptrend also remains strong. Prices have moved toward June 2015 levels and already breached our October 2017 long-term resistance levels, as per our Annual Outlook. Therefore, nickel prices remain in a strong uptrend and could continue increasing in the coming months.

Domestic Stainless Steel Market

Following the recovery in stainless steel momentum, domestic stainless steel surcharges increased this month. Surcharges remain above last year’s lows (under $0.4/pound); they remain in an uptrend, even if their pace has slowed. However, buying organizations may want to look at surcharges closely to reduce risks, either via forward buys or hedging.

[caption id="attachment_90273" align="aligncenter" width="580"] Source: MetalMiner data from MetalMiner IndX(™)[/caption]

Source: MetalMiner data from MetalMiner IndX(™)[/caption]

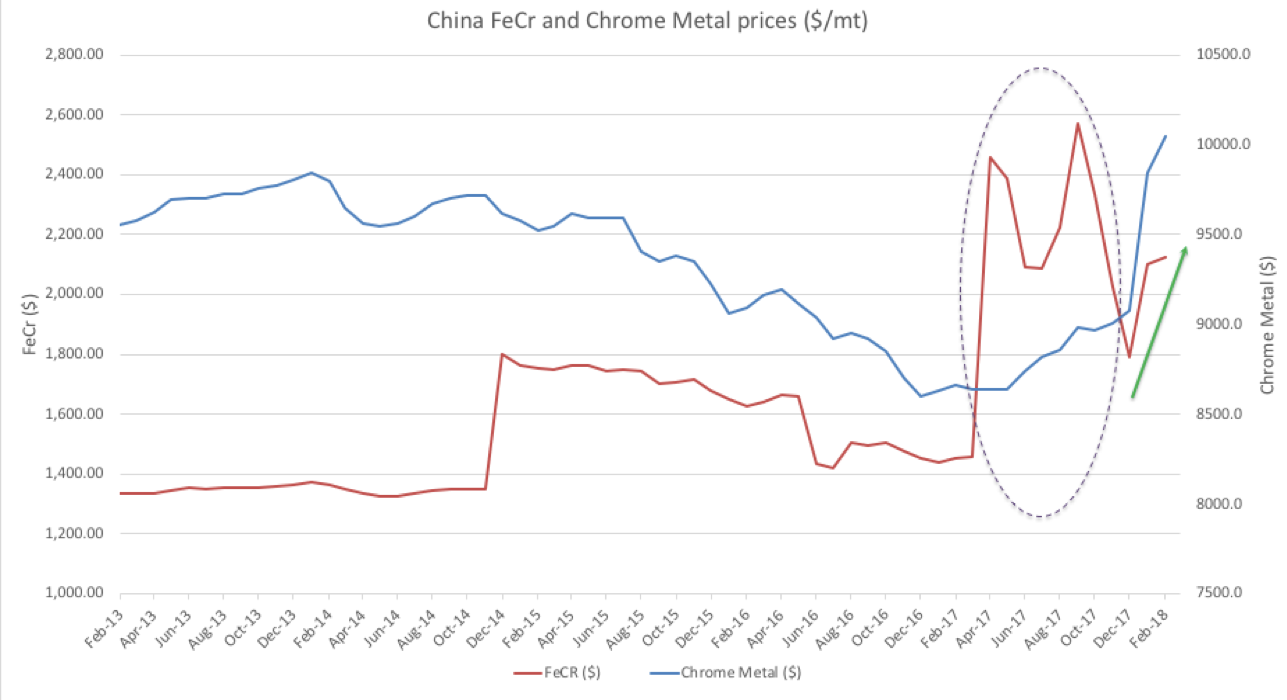

FerroChrome vs. Chrome Metal

Two months ago, MetalMiner reported on the anomaly between ferrochrome and chrome metal prices.

[caption id="attachment_90274" align="aligncenter" width="580"] Source: MetalMiner data from MetalMiner IndX(™)[/caption]

Source: MetalMiner data from MetalMiner IndX(™)[/caption]

Ferrochrome (FeCr) is a chromium and iron alloy containing 50% to 70% chromium by weight. Historically, Ferrochrome and chrome prices correlate tightly but the high iron ore prices caused ferrochrome to spike. However, both prices (ferrochrome and chrome) have fallen back to their historical trading pattern of moving together.

What This Means for Industrial Buyers

Stainless steel momentum appears in recovery, similar to all the other forms of steel. As both steel and nickel remain in a bull market, buying organizations may want to follow the market closely for opportunities to buy on the dips. To understand how to adapt buying strategies to your specific needs on a monthly basis, take a free trial of our Monthly Outlook now.

MetalMiner’s Annual Outlook provides 2018 buying strategies for carbon steel

Actual Stainless Steel Prices and Trends

This Morning in Metals: Aluminum Industry Testifies to ITC on Foil Imports

This morning in metals news, aluminum industry officials testified to the U.S. International Trade Commission regarding the ongoing aluminum foil investigation, Mexico’s economy minister says automotive rules of origin will change as part of the ongoing renegotiation talks surrounding the North American Free Trade Agreement (NAFTA) and copper is on track for its biggest weekly […]

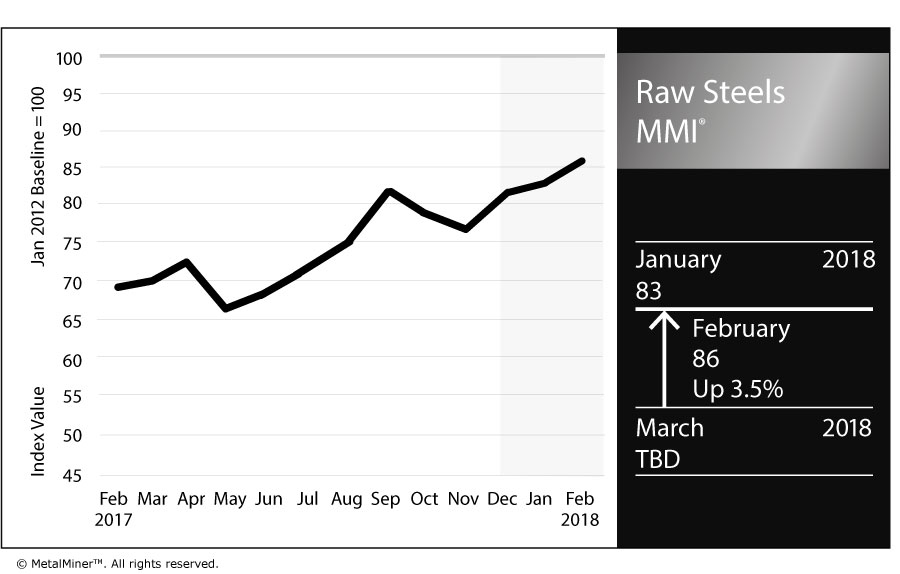

Raw Steels MMI: HRC Prices Hit Highest Level in More than Two Years

The Raw Steels MMI (Monthly Metals Index) inched three points higher this month, reaching 86 points.

Steel price momentum appears to have continued as prices increased sharply in January. February has already signaled a continuation of this uptrend, with HRC prices breaching the $700/st level. HRC prices have reached the highest levels in more than two years and could continue to climb.

Need buying strategies for steel? Try two free months of MetalMiner’s Outlook

[caption id="attachment_90232" align="aligncenter" width="585"] Source: MetalMiner data from MetalMiner IndX(™)[/caption]

Source: MetalMiner data from MetalMiner IndX(™)[/caption]

The spread between HRC and CRC prices fell this past month, returning to the $140/st level. Since the beginning of 2016, the spread between HRC and CRC prices increased to around $200/st. The spread has returned to normal levels, with HRC prices increasing more than CRC prices.

President Trump has yet to release results from the Section 232 investigation. Commerce Secretary Wilbur Ross sent his Section 232 steel report to Trump last month; the president has 90 days as of Jan. 11 to act on the report’s findings and recommendations.

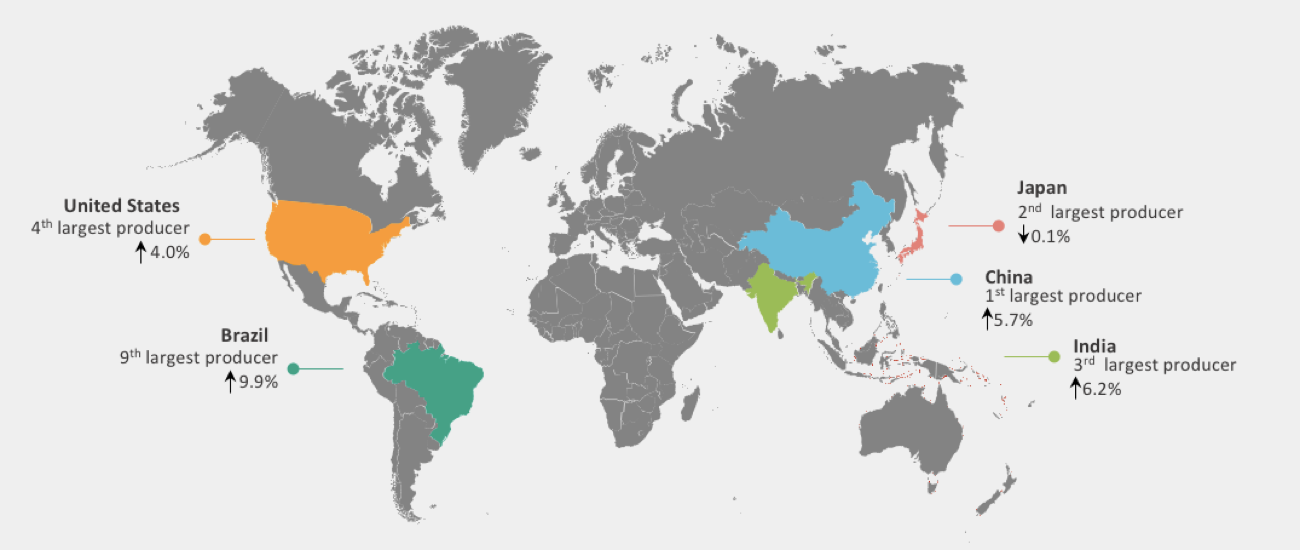

Global Steel Sector

According to the World Steel Association (WSA), global production of crude steel increased by 5.3% during 2017. The world map below reflects some of the changes in steel production by country and the impact on total steel output.

[caption id="attachment_90233" align="aligncenter" width="585"] Source: MetalMiner analysis of WSA data[/caption]

Source: MetalMiner analysis of WSA data[/caption]

Chinese global production of crude steel increased by 5.7%. However, China’s exports fell to 75.4 million tons last year from the previous 108.5 million tons. Japanese production of crude steel decreased by only 0.1%, while U.S. crude steel production increased by 4%.

According to Eurofer, European steel demand could increase by 1.9%. In 2017, European steel imports fell by 1% due to defensive trade measures.

Shredded Scrap

Shredded scrap prices increased again in January, shifting the latest short-term downtrend to an uptrend. The long-term uptrend remains in place, and scrap prices have now moved together with U.S. steel prices.

What This Means for Industrial Buyers

As steel price dynamics showed a strong upward momentum this month, buying organizations may want to understand price movements to decide when to commit mid- and long-term purchases. Buying organizations with concerns about the Section 232 outcome and its impact on the steel industry may want to take a free trial now to our Monthly Metal Buying Outlook. Our Monthly Outlook will include a detailed analysis of the Section 232 outcome.

For more efficient carbon steel buying strategies, take a free trial of MetalMiner’s Monthly Outlook!

Actual Raw Steel Prices and Trends

GOES MMI: GOES M3 Prices Fall Slightly as Imports Rise

The GOES MMI (Monthly Metals Index), which tracks, grain-oriented electrical steels, fell one point to 188 as other flat-rolled steel products saw a price increase.

Need buying strategies for steel? Try two free months of MetalMiner’s Outlook

Meanwhile, imports continue to grow, but none of the growth has come from China. In fact, Japan and the U.K. supplied the bulk of the imports in January. Buying organizations continue to report to MetalMiner they import grades of electrical steel not currently produced by the sole domestic producer, AK Steel. (See the latest import data below.)

[caption id="attachment_90225" align="aligncenter" width="585"] Source: International Trade Administration and MetalMiner Analysis[/caption]

Source: International Trade Administration and MetalMiner Analysis[/caption]

AK posted a Q4 loss but CEO Roger Newport made a number of comments regarding electrical steels during the most recent earnings call that indicated why the company supports strong Section 232 import measures:

“As we previously stated, we strongly believe that the ongoing high level of imports is a threat to the national security of our country…

Imports of grain oriented electrical steels, also known as GOES have more than doubled year-over-year and these imports are coming primarily from Japan, Korea and China. In my opinion this surge of GOES imports stems from a deliberate effort on part of these and other countries to beat the clock on any future 232 remedies and also by the Chinese trade protection causing Korea and Japan to send products to the United States.”

Unlike other steel products, such as tubular goods, cold-rolled steel, hot-dipped galvanized steel, solar panels and washing machines, MetalMiner is not aware of a single circumvention case for grain-oriented electrical steels.

Meanwhile, Bank of American Merrill Lynch analyst Timna Tanners double downgraded AK Steel on weak first quarter guidance and “lack of catalysts” to improve margins.

In Other Producer News…

ThyssenKrupp and Tata Steel have finally announced a joint-venture in Europe with the goal of becoming “a leading European flat steel provider and position it as a quality and technology leader,” according to a ThyssenKrupp press release. Both ThyssenKrupp and Tata have GOES production capability.

MetalMiner’s Annual Outlook provides 2018 buying strategies for carbon steel

Exact GOES Coil Price This Month

Copper MMI: Copper Prices Cool After December Surge

The Copper MMI (Monthly Metals Index) traded lower this month, falling one point for a February reading of 87. The fall was driven by a slight retracement of copper prices, which had skyrocketed in December. In January, LME copper prices fell by 1.21%.

Despite the price retracement, LME copper prices held above the $7,000/mt level at the beginning of February, and fell below this level during the second week. Trading volumes still support the uptrend. Copper prices could continue their rally.

Need buying strategies for copper in 2018? MetalMiner’s Annual Outlook has what you need

[caption id="attachment_90192" align="aligncenter" width="585"] Source: MetalMiner analysis of FastMarkets[/caption]

Source: MetalMiner analysis of FastMarkets[/caption]

Labor Disputes Could Threaten Copper Supply

Mine strikes continually threaten copper supply. BHP’s Escondida mine, the world’s largest copper mine, failed to develop a new labor agreement in advance of formal negotiations, scheduled for June. Last year, a 43-day strike at the Escondida mine impacted copper supply.

Since BHP’s Escondida copper mine produces around 5% of the world’s copper, it’s easy to see the impact of strikes on LME copper prices.

Meanwhile, Glencore forecasts its own copper output to increase by 150,000 tons at its Katanga mine in the Democratic Republic of Congo.

U.S. Dollar, Copper Back to Negative Correlation

Copper and the U.S. dollar maintain a strong negative correlation. The negative correlation gives the direction of the trends; when the U.S. dollar is weaker (downtrend), copper prices are stronger (uptrend).

The negative correlation did not hold during the first six months of 2017, nor did it hold for commodities and the U.S. dollar. However, the historical negative correlation has reappeared, as copper prices and the U.S. dollar now trade in opposition to one another.

[caption id="attachment_90193" align="aligncenter" width="585"] The U.S. dollar in black. Copper spot prices in purple. Source: MetalMiner analysis of StockCharts[/caption]

The U.S. dollar in black. Copper spot prices in purple. Source: MetalMiner analysis of StockCharts[/caption]

The U.S. dollar traded sideways during Q3 2017. Many analysts (not MetalMiner) started to believe the U.S. dollar had reached a bottom.

MetalMiner, however, remained more bearish on the U.S. dollar, as the dollar did not give any clear signs of a trend reversal. The distinction between a short-term trend that could impact prices in one to three months, versus a long-term trend, which could actually impact a buying strategy becomes important. The fact remains, the U.S. dollar has fallen to a more than three-year low.

Copper Scrap vs. LME Copper

In January, copper scrap prices did not move with the LME copper price. LME copper prices fell slightly, while copper scrap prices increased by 2%. Therefore, the spread between the two decreased slightly this month. We can expect these types of divergences in the short term, although the two tend to trade together over the longer term.

[caption id="attachment_90194" align="aligncenter" width="585"] Source: MetalMiner data from MetalMiner IndX(™)[/caption]

Source: MetalMiner data from MetalMiner IndX(™)[/caption]

In January, several Chinese copper scrap restrictions went into effect. The Ministry of Environmental Protection announced that only end-users and copper scrap processors will be allowed to import. This restriction in effect removes Chinese traders from the copper scrap market.

What This Means for Industrial Buyers

In January, buying organizations had some opportunities to buy some volume. The weak U.S. dollar and strength of other base metals support the bull narrative for copper. As long as copper prices remain bullish, buying organizations may want to “buy on the dips.” For those who want to understand how to reduce risks, take a free trial now to the MetalMiner Monthly Outlook.

Want to see an Copper Price forecast? Take a free trial!

Actual Copper Prices and Trends

Renewables MMI: Steel Plate, Cobalt Prices Post Sharp Increases

[caption id="attachment_88708" align="alignleft" width="300"] Chris Titze Imaging/Adobe Stock[/caption]

Chris Titze Imaging/Adobe Stock[/caption]

The Renewables MMI (Monthly Metals Index) skyrocketed this month, gaining 21 points en route to a 100 February reading.

Need buying strategies for steel? Try two free months of MetalMiner’s Outlook

The basket of metals posted price increases across the board, particularly in the steel plate category.

Japanese steel plate jumped 2.8%, while Korean steel plate rose 2.4%. Chinese plate jumped slightly, by 0.3%, and U.S. plate was up 6.5% as of Feb. 1.

Prices of neodymium, silicon and cobalt from China all posted significant price increases over the past month.

Scarcity of Critical Minerals to Threaten Renewable Industry?

According to a report from Stanford University, a scarcity in rare minerals could undercut the move toward greener forms of energy.

The topic was put forth for discussion at a mineral resources conference hosted by the university last month.

“Due to the rapidly increasing need for mineral resources as Earth’s human population continues to grow exponentially and the need to minimize the environmental and social impacts of mining, it’s essential that Stanford be involved in the field of economic geology — the study of the formation, exploration, and utilization of mineral resources,” said Gordon Brown, a professor of geological sciences at Stanford’s School of Earth, Energy & Environmental Sciences, as quoted in the report.

Uranium, copper, gold, lithium and rare earth elements (REEs) were among the materials cited in the report as critical to the future of renewable energy.

Among the trends impacting the supply of these valuable materials, according to the report, included: humanity’s increasingly growing rate of metal consumption, the concentration of rare elements in a relatively few countries, the quality (or lack thereof) of U.S. mineral mapping and reduction of mineral waste.

Cobalt Price Rises as Congo Seeks More Control of Market

Speaking of the concentration of minerals, the Democratic Republic of Congo is home to more than half of annual global cobalt production each year (in 2016, 66,000 of the 123,000 tons produced worldwide were sourced in the DRC, according to the U.S. Geological Survey).

Prices of cobalt are on the rise, shooting up a whopping 44.8% month over month.

With a number of international mining firms doing business in the DRC, the country’s largest state-owned mining company, Gecamines, is seeking to assert greater control of the market, Bloomberg reported.

“I find it scandalous that when cobalt is discussed, and the explosion of electric vehicles, only the traders and consumers are referenced and Congo and Gecamines are not cited,” Gecamines Chairman Albert Yuma was quoted as saying.

As reported by Reuters, Gecamines wants to renegotiate its contracts with foreign firms in order to work toward asserting further control of that cobalt market.

Cobalt is valuable for, among other uses, its application in electric vehicle batteries.

MetalMiner’s Annual Outlook provides 2018 buying strategies for carbon steel

Actual Metal Prices and Trends

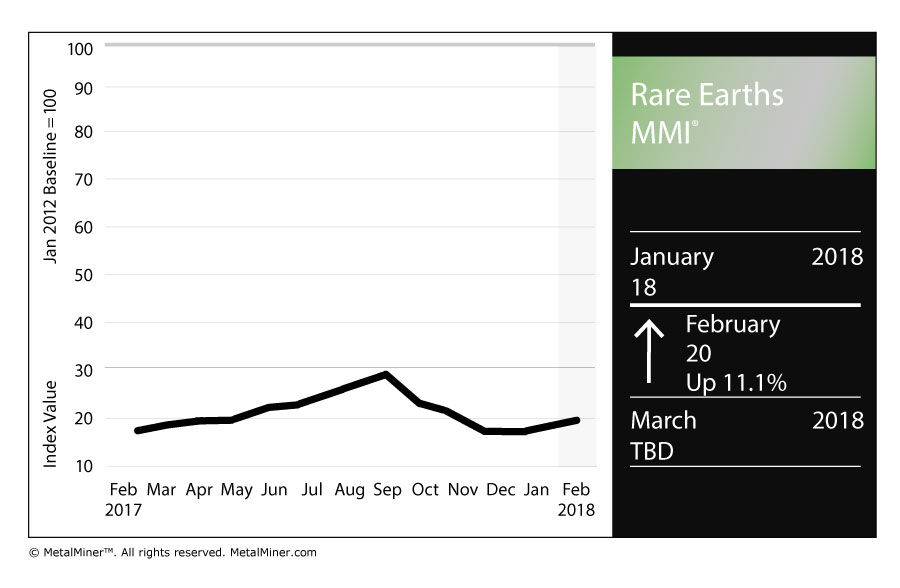

Rare Earths MMI: U.S. National Energy Technology Lab Works on Rare Earth Element Recovery Projects

The Rare Earths MMI (Monthly Metals Index) hit 20 for our February meeting, up from 18 last month.

Several of the heavier hitters in the basket of metals posted price increases this past month. Yttrium jumped 3.3%, while terbium oxide rose 12.4%.

Neodymium oxide surged 11.3% and dysprosium oxide rose 6.0%.

U.S. Lab Works to Increase Rare Earth Element Recovery

As we mention here every month, China has overwhelming control of the global rare earths market, meaning supply-side squeezes in the country often yield price spikes for the valuable materials used in things from electric vehicles to smartphones.

Unsurprisingly, the U.S. is looking for ways to increase its ability to recover rare earth elements (REEs) in domestic supplies of coal.

According to the National Energy Technology Laboratory (NETL), it is taking steps toward that goal.

“Four rare earth elements (REEs) recovery projects managed by the U.S. Department of Energy’s (DOE) Office of Fossil Energy and the National Energy Technology Laboratory (NETL) have made significant progress in the development of a domestic supply of REEs from coal and coal by-products by successfully producing REE concentrates,” a NETL release states.

The lab has run four test projects in different parts of the country. According to the release, the results of the projects are as follows:

-

Physical Sciences, Inc. (pilot-scale project) achieved 40 percent REE concentration at 15 percent REE recovery using post-combustion fly ash from burning Central Appalachian Basin coal. Field implementation and testing of physical processing technology will occur in Kentucky, with subsequent chemical processing in Pennsylvania.

-

The University of Kentucky (pilot-scale project) achieved greater than 80 percent REE concentration at greater than 75 percent REE recovery using Central Appalachian Basin and Illinois Basin coal preparation plant refuse. The project team plans to implement and test their technology at multiple field locations in Kentucky.

-

The University of North Dakota (bench-scale project) achieved 2 percent REE concentration at 35 percent REE recovery using North Dakota lignite coal. The University will build and test the technology in their laboratory.

-

West Virginia University (WVU) (bench-scale project) achieved 5 percent REE concentration at greater than 90 percent REE recovery using acid mine drainage solids from the Northern Appalachian and Central Appalachian Basins. WVU plans to build and test their unit in the WVU laboratory.

Of course, any new domestic capacity to recover REEs in the U.S. will be met with happiness by domestic end users, who have to pay a fortune for these rare and valuable materials.

Southeastern Alaska Town to be New Home of Rare Earths Plant

According to the a report in Mining News, the town of Ketchikan, Alaska, was chosen to be the new home of a rare earths processing facility.

Ucore Rare Metals Inc. picked the southeastern Alaska town for a new planned strategic metals complex (SMC).

“Engineering and economic studies have confirmed that Ketchikan is our preferred location to construct our first strategic and critical metals separation facility” said Mike Schrider, Ucore’s vice president of operations and engineering, in a company release. “Additional engineering and product specification criteria are being initiated at this time targeting rare earth by-products and primary concentrates from non-Chinese sourced projects world-wide. The intent is also to maintain the processing flexibility and capacity to accommodate ore concentrate from the Bokan-Dotson Ridge Project, once that project has been developed.”

According to the release, among other factors, Ketchikan’s proximity to the container port and rail head at Prince Rupert was cited as part of the locale’s desirability for the new SMC.

“Ketchikan features deep water port, barge-container facilities and direct access to markets in the US and the Pacific Rim by way of ocean vessel, the lowest-cost mode of bulk transport,” the release states. “Ketchikan offers a unique work force, ice-free harbors and is in close proximity to Ucore’s flagship in-situ development project, the Bokan Dotson-Ridge Rare Earth Project (“Bokan”).

Actual Metal Prices and Trends

Aluminum MMI: Aluminum Demand Gets Boost from Automotive, Aerospace Sectors

After last month’s sharp increase, the February Aluminum MMI (Monthly Metals Index) inched up one point.

The basket of metals increased despite the slight retracement of LME aluminum prices.The current Aluminum MMI index reads 99 points, 1.0% higher than in January.

In January, MetalMiner anticipated a possible retracement in aluminum prices, as aluminum — and, generally, all base metals — increased sharply at the end of the month. LME aluminum prices fell by 2.8% in January from the previous 2-year high closing price in December.

Buying Aluminum in 2018? Download MetalMiner’s free annual price outlook

[caption id="attachment_90155" align="aligncenter" width="580"] Source: MetalMiner analysis of FastMarkets[/caption]

Source: MetalMiner analysis of FastMarkets[/caption]

Aluminum prices inched lower during the first few days of February. Aluminum prices broke out of their previous sideways trend back in August, providing a strong buying signal. As prices may continue to increase, buying organizations may want to understand how to better purchase aluminum, reducing both risks and costs.

U.S. Domestic Aluminum Market

The U.S. Department of Commerce sent the Section 232 report for aluminum products to President Trump in January. President Trump has 90 days (from January 22) to review and announce actions regarding the probe for aluminum products.

Meanwhile, domestic aluminum demand received a boost from stronger U.S. automotive and aerospace sectors.

Despite the fall in U.S. auto sales in January, aluminum producers see increased demand. Demand has increased so significantly that Novelis Inc., the biggest flat-rolled products maker, announced the investment of a new plant in Kentucky to support growing automotive demand.

[caption id="attachment_90156" align="aligncenter" width="580"] U.S. Total Vehicle Sales. Source: TradingEconomics[/caption]

U.S. Total Vehicle Sales. Source: TradingEconomics[/caption]

Chinese Aluminum Market

SHFE aluminum prices currently trade lower than LME prices. Although the trends appear to be similar, SHFE aluminum prices fell further in January. Lower SHFE prices relative to LME aluminum prices lead to increased Chinese exports to Asia.

[caption id="attachment_90157" align="aligncenter" width="580"] Source: MetalMiner analysis of FastMarkets[/caption]

Source: MetalMiner analysis of FastMarkets[/caption]

According to the latest Chinese customs data, Chinese exports of unwrought aluminum and aluminum products increased by 12.8% in December compared to December 2016 data. December exports also increased on a monthly basis by 15.8% over November’s figures.

Aluminum Premiums

U.S. Midwest aluminum premiums moved again at the beginning of February, and currently trade at $0.12/pound. The Section 232 investigation and uncertainty around the outcome has increased the volatility in the U.S. Midwest premium.

Other aluminum delivery premiums also increased this month. The CIF Japanese spot premium increased 12% over January, to $98.50-$110/mt from the previous $90-96/mt. The European duty-unpaid premium jumped by 8.1%, while the Brazil CIF duty-unpaid premium increased by 3%.

What This Means for Industrial Buyers

As expected after last month’s sharp increase, aluminum prices retraced in January. In bullish markets, buying organizations still have many opportunities to forward buy. Therefore, adapting the “right” buying strategy becomes crucial to reduce risks.

Want to see an Aluminum Price forecast? Take a free trial!

Actual Aluminum Prices and Trends