Speculators may love volatility, but metal buyers hate it. As for Trump Tariffs 2025, the jury is still out. The truth is that a bout of unexpected turbulence like we’ve seen over the last couple of months can knock even the best-laid strategies sideways. The reasons are clear: markets nosedived in March and hit bottom […]

Category: Supply & Demand

Rare Earths MMI: Ukraine and U.S. Strike Critical Minerals Deal

The Rare Earths MMI (Monthly Metals Index) witnessed a significant rise in price action month-over-month, with a total increase of 7.67%. So far, the global rare earths market has been on a springtime rollercoaster. Between April 1 and May 2, 2025, prices for these critical elements saw abrupt swings, supply chains were tested by geopolitics […]

U.S. Aluminum vs. European Aluminum: A Comprehensive Short-Term Market Outlook

A striking aspect of the aluminum premium and the aluminum market turmoil currently unfolding after Trump’s aluminum tariffs is how differently it’s playing out in the U.S. versus other regions. While premiums inside of the U.S. are rising, outside the United States, aluminum premiums are actually falling. With U.S. tariffs shutting out or discouraging some […]

Aluminum Delivery Premiums Spiking After Tariffs, are Aluminum Freight Bottlenecks Coming?

In the past month, the cost of importing aluminum into the United States has risen sharply. This occurred as aluminum market delivery premiums, the added charges above the base metal price for physical shipments, came close to record highs. This surge in costs stems primarily from a combination of fresh U.S. tariffs, global shipping delays, […]

Construction MMI: China Tariffs Climb to 145%. What it Means for China-Sourced Construction Materials

The Construction MMI (Monthly Metals Index) broke out of its over 6-month-long sideways trend to pivot down 5.41%. This new movement outside of its sideways range could indicate more volatility in the short term than the index experienced in the past 12 months. The new Trump tariffs on China caused some volatility in the price […]

Aluminum MMI: How Suppliers Handle Tariffs and What Aluminum Buyers Need to Know

The Aluminum Monthly Metals Index (MMI) remained sideways, as most components appeared consolidated. Overall, the index slid 0.74%, while aluminum prices experienced continued instability. Aluminum Price Volatility After Tariffs Aluminum prices have appeared increasingly volatile since the announcement of tariffs. Prices plunged after reaching a mid-March peak, breaking below their sideways range. The implementation of […]

Copper MMI: What’s Next for Copper Prices After Peak

The Copper Monthly Metals Index (MMI) moved up, accelerating gains from the previous month. The Bullish U.S. price of copper saw the index rise by 4.75% from March to April. Price of Copper Finally Finds Peak Although they have subsequently been delayed, reciprocal tariffs helped copper prices find a peak. At the start of 2025, […]

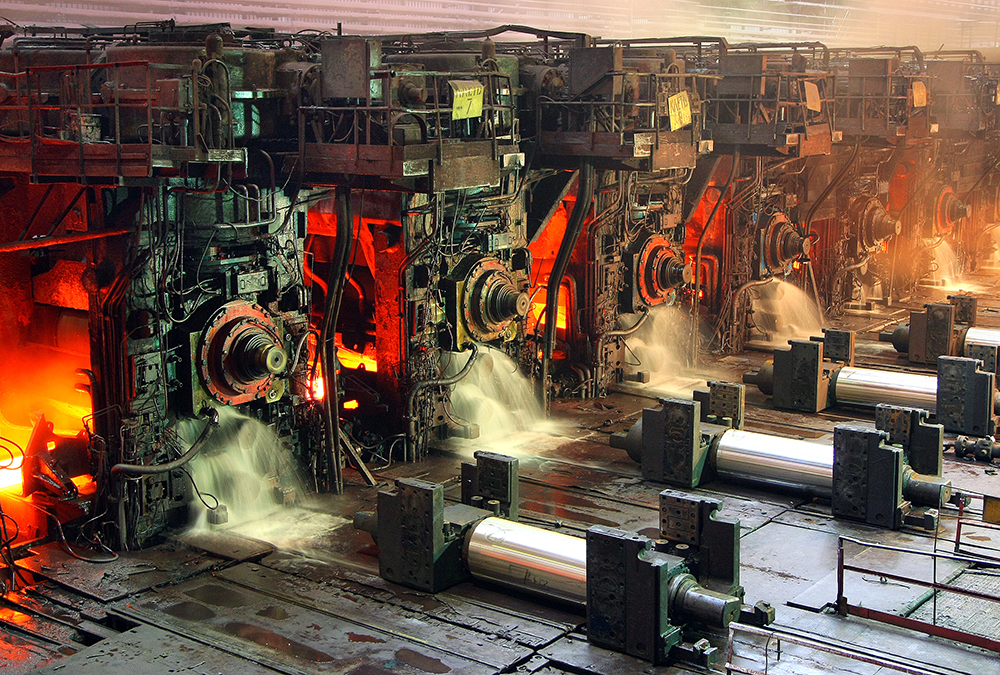

Raw Steels MMI: Steel Prices Level Off, Lead Times Shrink

The Raw Steels Monthly Metals Index (MMI) returned to the downside. Overall, the index witnessed a modest 0.75% decline from March to April. Steel Prices Find Peaks as Reciprocal Tariffs Spare Steel Steel prices either found a peak or began to stabilize by the start of April. As of April 4, hot rolled coil prices […]

Rare Earths MMI: Rare Earths Market Rattled by Myanmar Earthquake and Tariffs

The Rare Earths MMI (Monthly Metals Index) moved sideways, edging up by a slight 1.82%. The global rare earth market has taken a significant hit lately, thanks to a combination of natural disasters and big geopolitical moves. A strong earthquake in Myanmar and the recent wave of U.S. tariffs have thrown this somewhat delicate industry […]

China Just Redrew the Aluminum Map, and the World Is Watching

At a time when analysts expect the global demand for aluminum to rise, a new development in China may significantly impact both aluminum market demand and the country’s internal consumption. That said, market watchers know that any announcement around metals coming out of Beijing these days also has to be looked at through the lens […]