The Stainless Monthly Metals Index (MMI) moved sideways with a modest 1.41% decline from October to November. All in all, the stainless steel price movement primarily reacted to volatility in nickel trading. Nickel held historically low volume levels over recent months, while nickel prices remained within their short-term range. By November, however, prices began to […]

Tag: stainless steel price

Stainless MMI: Nickel Prices Down After Bullish Month

By: Nichole Bastin and Katie Benchina Olsen The Stainless Steel Monthly Metals Index (MMI) rose 3.35% from September to October. Last month, nickel prices traded up with a strong rebound during the first three weeks. However, prices soon fell back within range. These declines continued until the opening days of October, with prices mainly remaining […]

Stainless Steel MMI: Nickel Prices Move Sideways, Begin to Climb in September

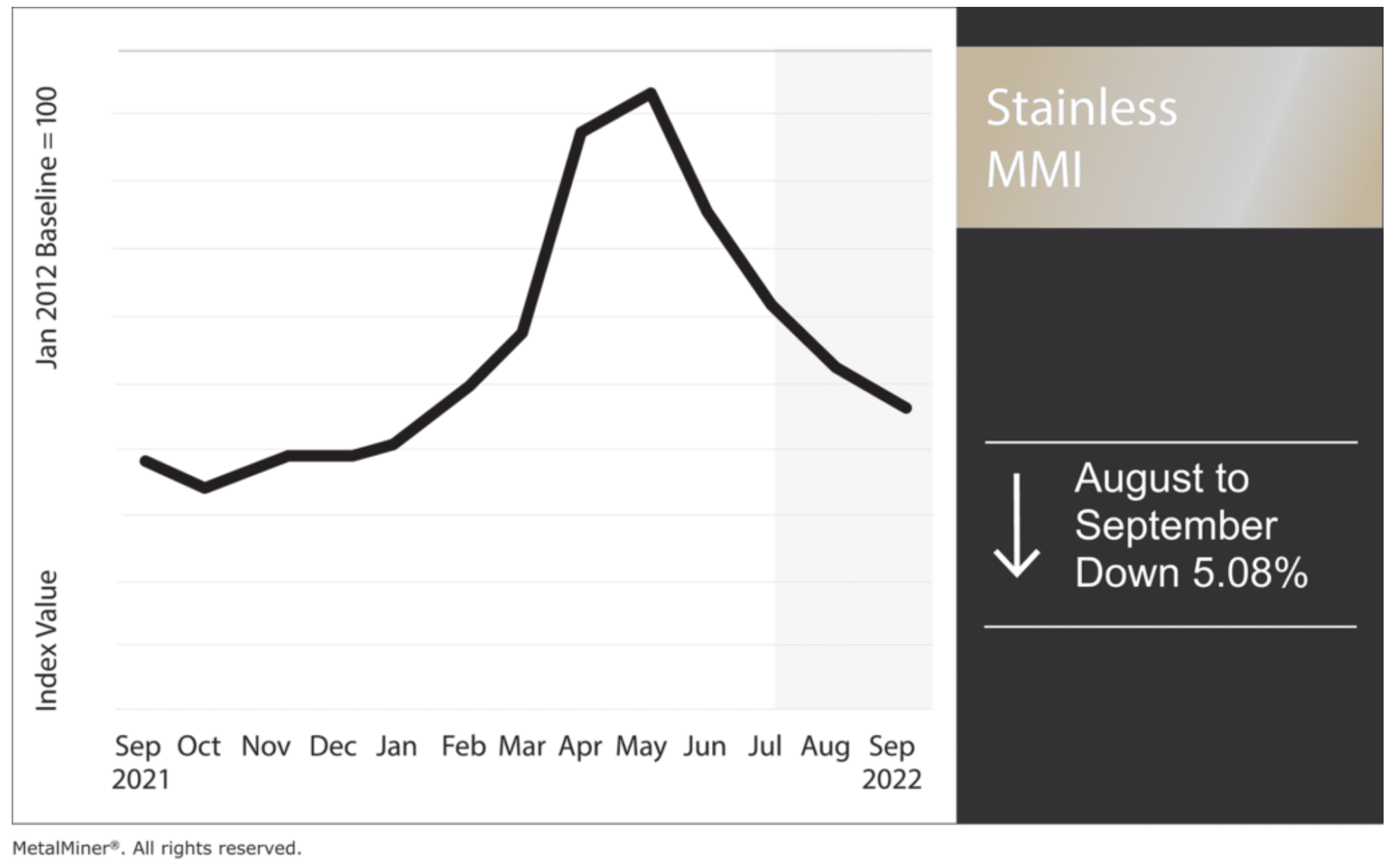

By Nichole Bastin and Katie Benchina Olsen The Stainless Steel Monthly Metals Index (MMI) dropped 5.08% from August to September. Nickel prices began to rise this month, breaking through prior highs visible on shorter time frames such as the hourly and daily charts. Ultimately, prices bounced off bullish zones formed before the LME’s shutdown in […]

Stainless Steel in a “Commodity Standoff”

Stainless steel prices continue to struggle as we approach the final quarter of the year. Meanwhile, nickel prices float just above their 2021 average, closing August at $21,320 / mt. Both indices seem to indicate an overly-cautious marketplace, with buyers and sellers seemingly waiting to see what the other will do. This sort of “commodity” […]

Stainless MMI: Nickel Prices Fall to a 6-Month Low

The Stainless MMI continues its decline this month. Moreover, nickel prices continue to show weakness without any apparent bullish anticipation from market participants. As the entire industrial metals market sloped downward, nickel prices followed suit. Moreover, volumes remain lower than pre-LME shutdown levels, which will continue to foster slow price movement. The Stainless Monthly Metals […]

Estimating Stainless Steel Costs Becoming More Complicated

Last Month, MetalMiner reported that stainless steel cost had been holding strong amid high demand and increased production. However, we did identify some cracks in what might otherwise look like a solid recovery. As we transition from Q2 to Q3, some of those cracks have grown significantly. Low Demand in China Affecting Stainless Steel Cost […]

Nickel Prices: LME Nickel Contract Continues to Lack Liquidity, Harming Price Discovery

Nickel prices are seeing a lot of attention due to an overall lack of liquidity on the LME contract. But what exactly does this mean? Moreover, what does it mean for buyers looking to mitigate price problems in the face of global supply problems? The metals market moves fast. Sign up for the weekly MetalMiner […]

Stainless Steel MMI: Stainless Prices Holding Strong

The Stainless Steel MMI indicates that prices are holding fast. This, as cold-rolled stainless imports to the U.S. have averaged above 40,000 MT per month for several straight months. Meanwhile, U.S. flat-rolled stainless producers have run at full capacity for over a year now. Still, they continue to place premiums on products they simply don’t […]

Stainless MMI: Nickel prices trade down but remain elevated amid lower LME volumes

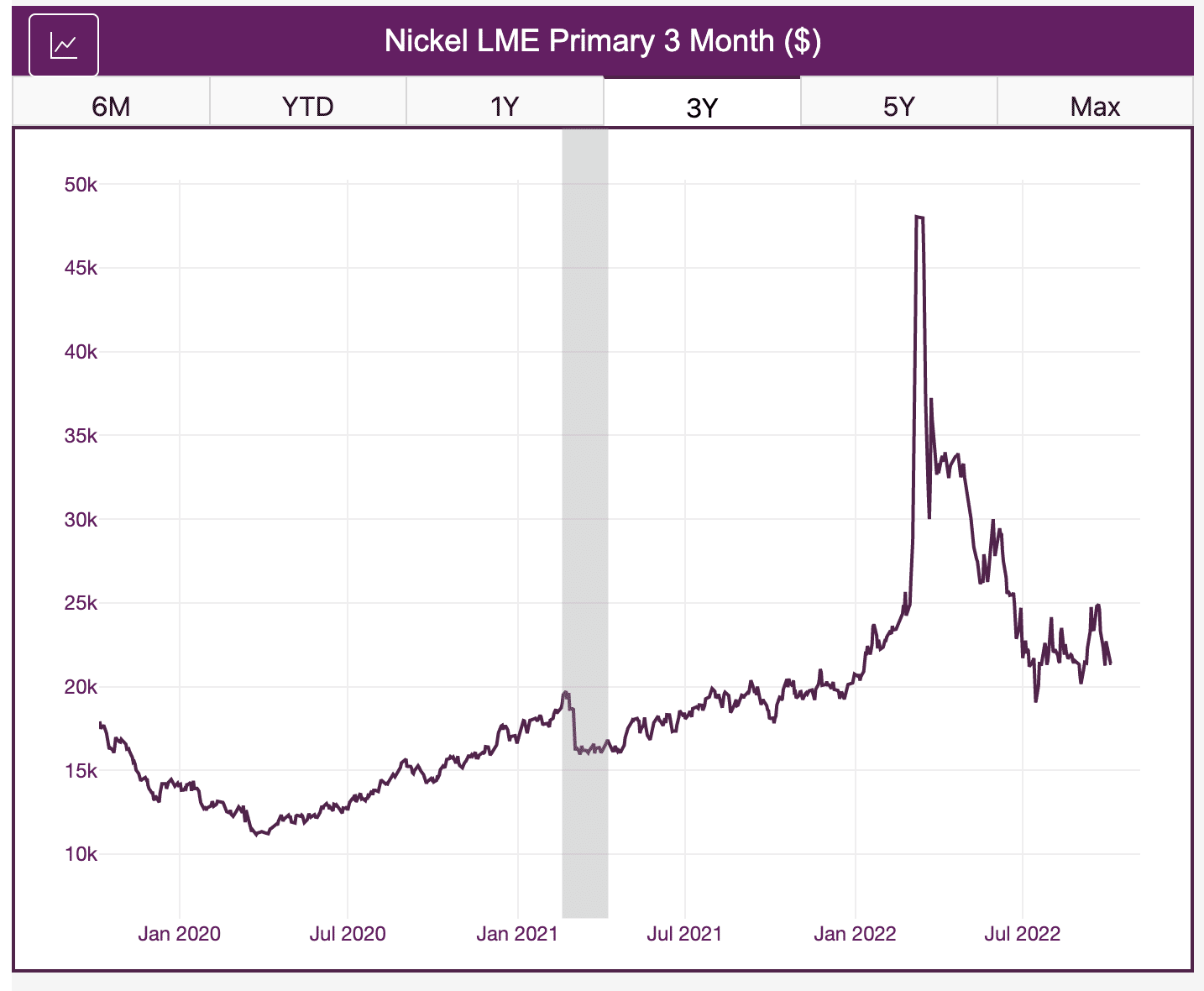

The Stainless Monthly Metals Index (MMI) jumped by 25.07% from March to April, as nickel prices remained elevated. Nickel prices continue to trade slightly downward. However, nickel prices remain elevated from pre-invasion levels. Volume flow fluctuated among exchanges in recent days due to distrust of the LME, while nickel prices began to trade within an […]

Stainless MMI: Trading halted following nickel price spike

The Stainless Monthly Metals Index (MMI) rose by 7.6% from February to March, as the skyrocketing nickel price prompted LME intervention Tuesday. LME suspends trading due to short squeeze Russia accounts for roughly 7% of global nickel supply. So, the possibility for supply disruptions, on the back of mounting sanctions from the West, adds pressure […]