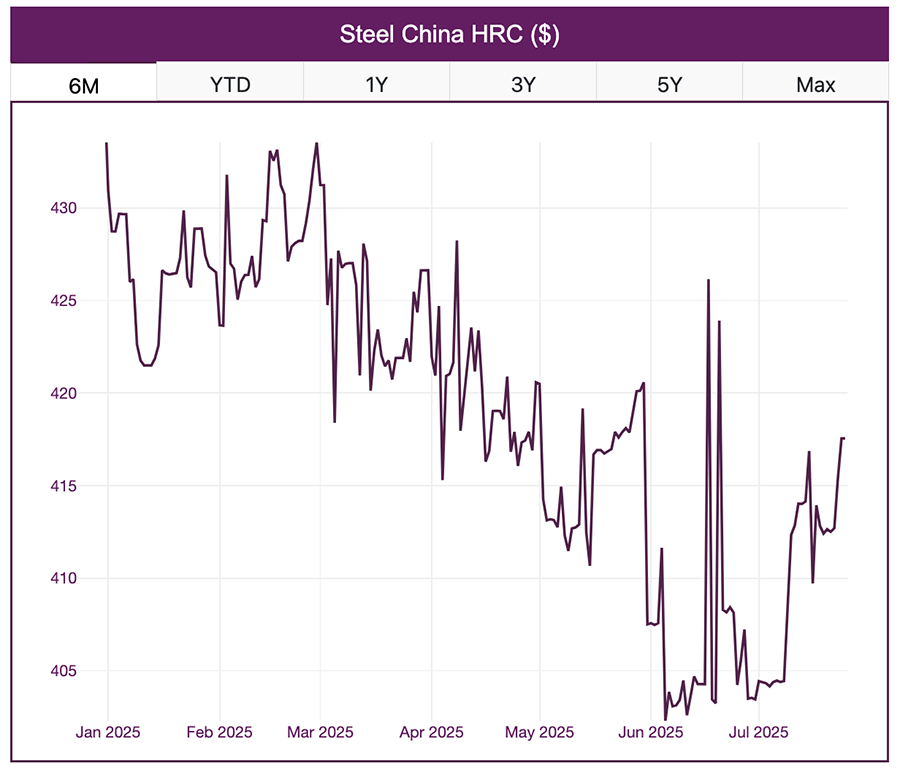

Can China’s Steel Rally Outrun Its Struggling Property Market?

In the end, China exceeded market expectations, posting a 5.2% year-on-year growth on July 14 compared to the market forecast of 5%. According to the economic data released by the National Bureau of Statistics, strong trade and industrial production helped to propel growth, indicating that China has braved the tariff war unleashed by the United States. Meanwhile declining steel prices seem to indicate further trouble in the property market.

Want to enhance your steel market intelligence? Subscribe to MetalMiner’s Monthly Metals Index Report to gain a deep understanding of the dynamics affecting steel prices and markets, along with seven other metal industries.

A Strong Monday Showing for Iron Ore

It was this very expectation of a 5% growth in Q2 that iron ore traders were banking on. In the days leading up to the release of the Q2 data, iron ore wrangled its biggest weekly gain since January this year. This came as presumptuous traders bet on the positive reporting of the second-quarter economic growth by the world’s largest metals-consuming nation.

Last Monday, the future prices of this steel raw material rose to as high as $99.90 a ton after surging 3.6% the previous week. Following the biggest gain in recent months, the ore futures market continued to rally. Singapore iron futures hovered near the US $99.30 ton mark while the yuan-dominated contracts on the Dalian exchange advanced. This contrasted with a decline in steel futures on the Shanghai markets.

A Tuesday Retreat

The script was slightly different when markets opened on Tuesday. Following the release of China’s economic growth data, markets saw a significant dip. As weak property sector data from China dented market sentiment, benchmark 62% iron ore futures fell. Futures on the Singapore Exchange dropped toward $105 per tonne, with Dalian prices also retreating.

By the end of Tuesday trading, iron ore futures had fallen by 1.6%, indicating slowing demand from steel companies. In Singapore, ore price settled at US $98.92 per ton, down by 0.7%. Meanwhile, according to this report, Dalian (yuan-based) and Shanghai (steel contracts) also reported a decline in futures rates.

Turn steel market jitters into cost-saving opportunities. Subscribe to MetalMiner’s newsletter.

Amid Falling Steel Prices, China May Move to Curb Capacity

As revealed in the new set of economic data, declining steel prices could be a direct fallout of sharper-than-expected slowdowns in fixed-asset investment, retail sales and falling property prices. In June, new home prices in China fell for a 12th consecutive month. There’s also concern that a slowdown could be on the way, even though Beijing claims its economy is on track.

Incidentally, much of the rally in iron ore futures last week was due to anticipation that China would announce schemes to boost the ailing property sector and counter industrial overcapacity. While the former did not happen, the data released contained some indication that the latter may still be in the works.

Going forward, analysts say iron ore gains are narrowing as traders grow cautious amid high prices, which they expect to hover between $95–100/ton in the short term. Meanwhile, some primary market drivers include continued resilient demand from Chinese steel mills despite production cuts, declining sea shipments from Australia and Brazil, trader optimism and port inventories continuing to fall, indicating strong consumption.

Steel Down Alongside Property

According to this report, June steel production decreased 9.2% year-over-year to 83.2 million tons, marking the largest monthly decline in 10 months. China’s economic growth eased slightly in Q2 2025, registering a year-on-year expansion of 5.2%, a decline from 5.4% in Q1. Despite the moderation, the second-quarter performance surpassed market consensus, even after analysts raised forecasts in May.

For the first half of the year, China’s GDP rose by 5.3% YoY, keeping the country on course to meet its “around 5%” growth target for 2025. Nevertheless, first half output is now at its weakest since 2020, 3% below last year’s pace. For now, Beijing appears ready to continue its efforts to curb oversupply in key industrial commodities, and the data released suggests continued pressure on the construction and manufacturing sectors amid a broader economic slowdown.

What Does the Future Hold?

Looking ahead, the second half of 2025 presents new headwinds for China’s economic growth, which is obviously going to affect iron ore costs, steel prices and more. This analysis suggests that tariff-related uncertainty remains a significant overhang, particularly as critical deadlines approach in August. While a return to April’s peak tariffs seems unlikely, further escalations can’t be ruled out. This would potentially suppress investment and weigh on business confidence.

Additionally, momentum from trade-in subsidies may start to taper unless policies are further extended. Efforts to tackle China’s “involution”—excessive price competition—could deliver long-term gains, but not without near-term economic friction.

Despite these challenges, the solid first-half showing leaves China well-positioned to meet its full-year growth target .According to the report by the research team at ING, current risks to the 4.7% YoY GDP forecast appear broadly balanced, with some upside potential,

Do you know which steel contracting mechanisms are best with different market conditions? Check out our best practices on this topic.