The best metal buying teams are not flashy. They are disciplined. So what are the top metal price forecasting tools? They are the ones that clearly define exposure and price risk, follow a calculated process, and make decisions before markets force their hand. Over time, that discipline matters more than any single metal buy. Historical […]

Tag: Aluminum

How Does MetalMiner’s Forecasting Engine Help You Make Better Sourcing Decisions?

Procurement and finance teams have many opinions about the direction of metal prices. However, what they sometimes lack is a clear and structured approach to turn market noise into knowledge about optimal purchasing windows. This is where MetalMiner, Sage, and Market Signal come in. MetalMiner is not meant to replace judgment. It aims to organize […]

Aluminum MMI: Aluminum Prices Hit 6-Month High

The Aluminum Monthly Metals Index (MMI) remained sideways with an upside bias, rising 0.56% from August to September. Meanwhile, the global price of aluminum reached highs not seen since the beginning of the year. Track other MetalMiner monthly indexes here, and compare how the overall industrial metal market is performing. Worried about the fluctuating price […]

Will Demand Drive a $126 Billion Bauxite Market by 2033?

Despite a few hiccups and occasional worries of oversupply, the global bauxite market has been growing steadily. Much of this expansion has been fueled by rising demand in the aluminum market, especially from automotive, aerospace and renewable energy sectors. About 60% of EV manufacturers and over 70% of aerospace materials use aluminum in one form […]

Aluminum Prices Continue to Hold Steady Amid Global Supply Constraints and Infrastructure Push

Recent movements in aluminum prices show the metal holding strong despite global economic shifts and region-specific challenges in extraction and refining operations. On July 25, aluminum prices on the London Metal Exchange climbed to a four-month high, ending the week at US $2,656.5 and US $2,657 per ton, an increase of $10.5 or 0.39%. According […]

Aluminum MMI: MW Premium Finds New High

The Aluminum Monthly Metals Index (MMI) remained sideways with an upside bias. Overall, the index rose 1.99% from June to July as aluminum prices slowed their ascent. Track other MetalMiner monthly indexes here, and compare how the overall industrial metal market is performing. Midwest Premium Returns to the Upside Stabilization proved temporary for aluminum’s Midwest […]

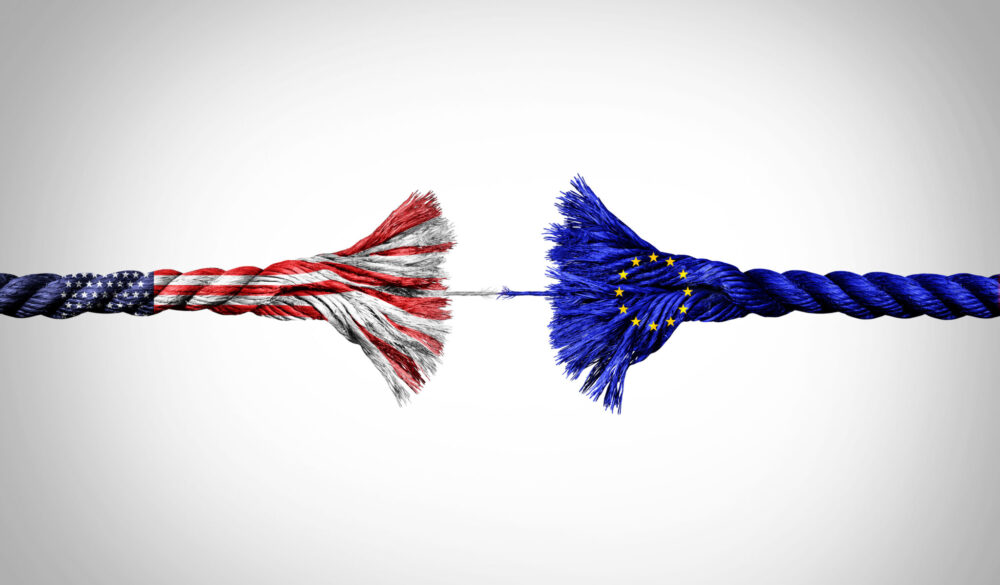

Steel Showdown: EU Warns Retaliation as Trump Doubles Down on Tariffs

The European Commission (EC) has expressed concern about Donald Trump’s announcement of plans to double import tariffs on steel. The U.S. President proclaimed the new “Trump Tariffs” during a speech at US Steel’s Mon Valley-Irwin works in Pennsylvania on May 30. “We strongly regret the announced increase of U.S. tariffs on steel imports from 25% […]

Tariff Ticking Time Bomb: Trump Gives UK Until July 9th to Avoid Steel Shock

Trump tariffs are back once again putting U.S trade partners in a tough spot. President Donald Trump recently exempted the United Kingdom from his doubling of import tariffs on steel and aluminum into the United States, but only temporarily. While import tariffs from UK steelmakers remain at 25% for now, failure to reach an agreement […]

China’s Metal Anti-Dumping is Back. What You Need to Know

Chinese mills are churning out steel, aluminum and even refined copper at near-record levels and sending the surplus abroad, a trend steel industry analysts say could pressure industrial metal prices in the United States. After a year of lagging domestic demand, China’s exports of construction and manufacturing metals have surged, flooding global markets with cheap […]

Aluminum MMI: Aluminum Prices Stabilize as Midwest Premium Hold onto Gains

The Aluminum Monthly Metals Index (MMI) appeared increasingly bearish with a 3.08% decline from April to May. What do other metal and commodity market trends mean for aluminum trends? Track other MetalMiner monthly indexes here, and compare how the overall industrial metal market is performing. Aluminum Prices Stabilize Following Post-Tariff Drop Aluminum prices found an […]