The Raw Steels Monthly Metals Index (MMI) accelerated during the month, moving up 3.87% from July to August as steel prices continued to slide. U.S. Steel Prices Continue Slow Downtrend U.S. steel prices have remained within a slow but steady downtrend since their late-March peak. As of mid-August, prices were down 9.49%, falling to their […]

Category: MetalMiner IndX

MetalMiner’s IndX

Stainless MMI: Indonesia Looks to Support Nickel Prices

The Stainless Monthly Metals Index (MMI) remained sideways, retreating by a modest 2.64% from December to January. All of the index’s components trended lower, weighed down by bearish nickel prices throughout the month. Indonesia to Address Nickel Supply Glut Indonesia is currently eyeing substantial output cuts after nickel prices descended beneath the $15k/mt mark. High […]

Renewables/GOES MMI: Renewable Resources and the “Surprise Climate Bill”

The Renewables MMI (Monthly Metals Index) continued its downward trend this month, falling an additional 7.10% between July and August. However, this trend is not likely to continue if the US senate passes the so-called “surprise climate bill.” Were this to happen, it would put fresh focus on renewable resources, likely causing the MMI adopt […]

Aluminum MMI: Aluminum Prices Consolidate 39% Beneath March Peak

After seeing a short-term bullish rebound in July, aluminum prices began to modestly decline again in early August. All in all, the rebound was insufficient to suggest a bullish reversal. As such, global aluminum prices remain within a macro downtrend despite recent directional uncertainty. The Aluminum Monthly Metals Index (MMI) dropped by 2.4% month over […]

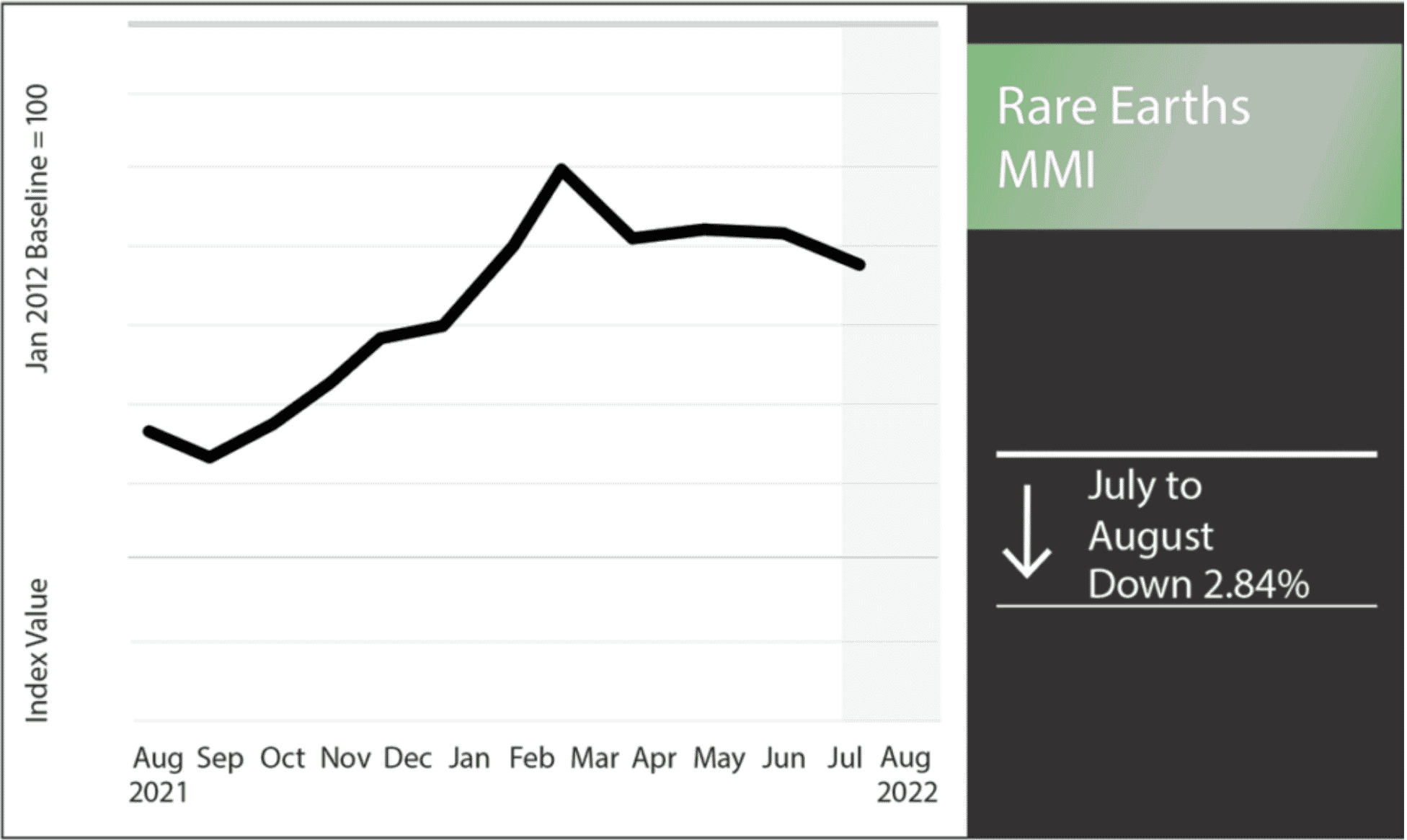

Rare Earths MMI: Rare Earth Prices Slide Further as World Looks for New Supplies

The Rare Earths MMI (Monthly MetalMiner Index for rare earth metals) extended its decline in July, dropping another 2.8%. This is a significant move for rare earths prices, and reinforces the subtle downtrend that began back in April. Now more than ever, countries are frantically searching for ways to separate their rare earths supply from […]

Rare Earths MMI: US and China Feud Over Rare Earth Prices

Over the past month in, the Rare Earths MMI (Metal Miner Index) slightly dropped by 0.64%.Over the past few decades, the US-China relationship has evolved into more of a rivalry than anything else. This has left the United States eager to decouple from China on several critical issues. One such issue is the supply of […]

Core Loss the Center of Grain-Oriented Electrical Steel Exclusion Requests

For large power equipment manufacturers, Section 232 comes down to two little words: core loss. Nobody explains the situation better than SPX Transformer Solutions in their Section 232 exclusion request for two grades of domain-refined GOES: “DR-GOES is one of the most expensive materials used in the manufacture of power transformers, and its cost equates […]