The impact of the president’s Section 232 proclamation applying a 25% import duty on all steel articles with HTS codes 7206.10 through 7216.50, will have a somewhat predictable impact on steel prices (they will increase, at least in the short term).

Need buying strategies for steel? Try two free months of MetalMiner’s Outlook

The impact on grain-oriented electrical steel (GOES) buying organizations, MetalMiner believes, will not exactly mirror the broader impact of the tariffs on commonly purchased steel forms, alloys and grades.

But first, the reaction to the announcement of the steel tariffs from Roger Newport, the CEO of AK Steel, and the last remaining GOES producer in the U.S.: “We support President Trump for taking the bold action of imposing a 25% global tariff on steel to defend America’s steel industry and its workers from imports that threaten our national and economic security,” he said. “Nowhere is this threat more evident than in electrical steel where AK Steel is now the only domestic producer of electrical steel for electrical transformers. Years of surging imports and the subsequent market volatility caused the only other U.S. producer to exit the market in 2016. This action by the President could not come soon enough as the surge of electrical steel imports continued throughout last year, with imports nearly doubling in 2017 when compared to 2016.”

GOES Markets Are More Nuanced Than Other Flat Rolled Products Markets

GOES markets serve as an example of where and how certain sub-segments of the steel industry will attempt to carve out exceptions and/or exemptions from the tariff proclamation — specifically, under point 11 of Trump’s proclamation.

MetalMiner believes that Japanese producers, along with their importing partners and customers, will petition the Department of Commerce for an exception by proving that certain highly engineered grades of electrical steel are not in fact produced in the United States.

The president’s proclamation identifies the procedure by which exceptions can be made:

The Secretary, in consultation with the Secretary of State, the Secretary of the Treasury, the Secretary of Defense, the United States Trade Representative (USTR), the Assistant to the President for National Security Affairs, the Assistant to the President for Economic Policy, and such other senior Executive Branch officials as the Secretary deems appropriate, is hereby authorized to provide relief from the additional duties set forth in clause 2 of this proclamation for any steel article determined not to be produced in the United States in a sufficient and reasonably available amount or of a satisfactory quality and is also authorized to provide such relief based upon specific national security considerations. Such relief shall be provided for a steel article only after a request for exclusion is made by a directly affected party located in the United States.

Clearly, the impact of imports on the domestic GOES market has come on the back of rising and significant Japanese imports. China and South Korea are non-players for GOES into the U.S.

[caption id="attachment_90783" align="aligncenter" width="580"] Source: International Trade Administration and MetalMiner Analysis[/caption]

Source: International Trade Administration and MetalMiner Analysis[/caption]

The real question involves whether or not customers of Japanese products will be able to prove that the materials they are buying from Japan, are indeed not produced in the U.S.

The president has mandated that the secretary of commerce issue procedures for requests for tariff exclusions within 10 days of the proclamation date (which was March 8).

MetalMiner’s Annual Outlook provides 2018 buying strategies for carbon steel

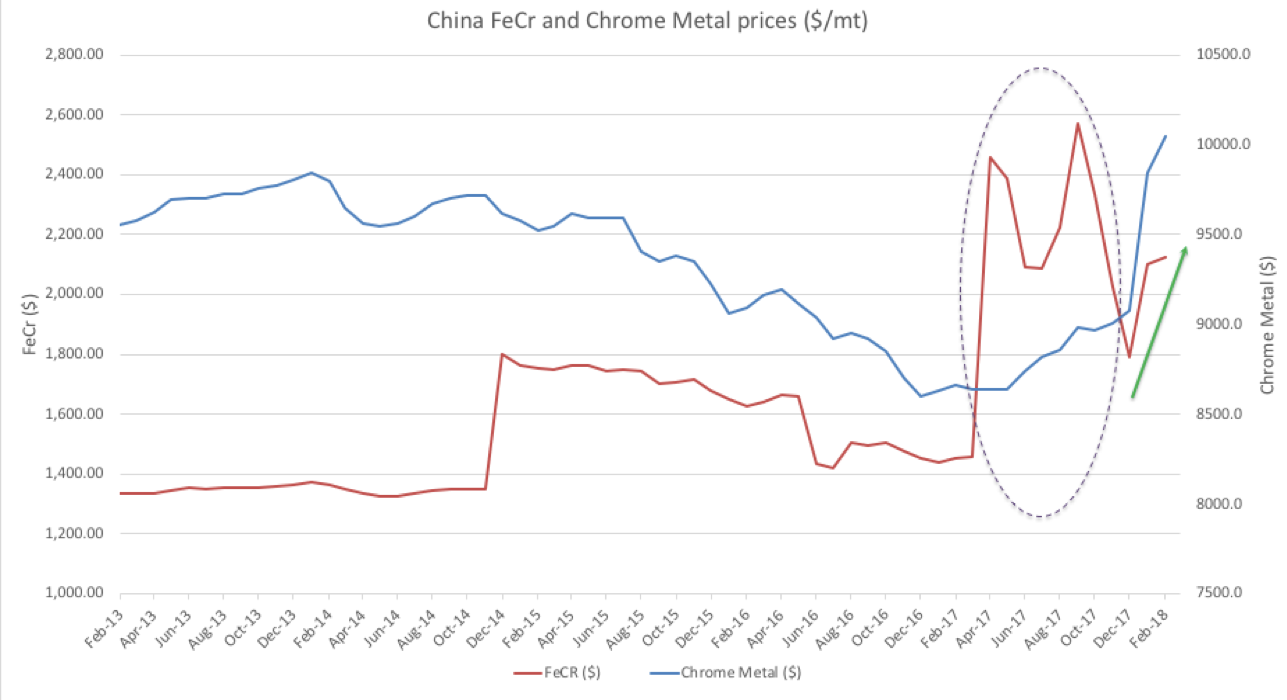

Exact GOES Coil Price This Month