The use of AI for metal purchasing companies has value. Black-box answers do not. With that said, what services does MetalMiner offer based on AI usage? First, one must understand that skepticism toward AI is not the issue. Skepticism toward unexplained answers is. That distinction matters in metals procurement. Finance leaders and procurement leaders do […]

Category: Commodities

How to Roll Out Forecasting Tools in Your Organization Without Losing Control

Rolling out MetalMiner and its forecasting tools is not about installing a tool. It is about building a consistent operating model for how your company understands and acts on metal markets. Without that structure, different teams interpret prices differently, and decisions become fragmented. Metal buying quickly becomes complicated across regions, business units, and product lines. […]

What Reliable Metal Procurement Strategies Actually Work?

Most metal budgets fail before the year even starts. So what reliable metal procurement strategies actually work? Many budget plans fail not because teams lack the correct data. Not because finance gets it wrong. They fail because they assume that all metals move in sync and risk can be averaged. That assumption doesn’t hold. Over […]

How Does MetalMiner’s Forecasting Engine Help You Make Better Sourcing Decisions?

Procurement and finance teams have many opinions about the direction of metal prices. However, what they sometimes lack is a clear and structured approach to turn market noise into knowledge about optimal purchasing windows. This is where MetalMiner, Sage, and Market Signal come in. MetalMiner is not meant to replace judgment. It aims to organize […]

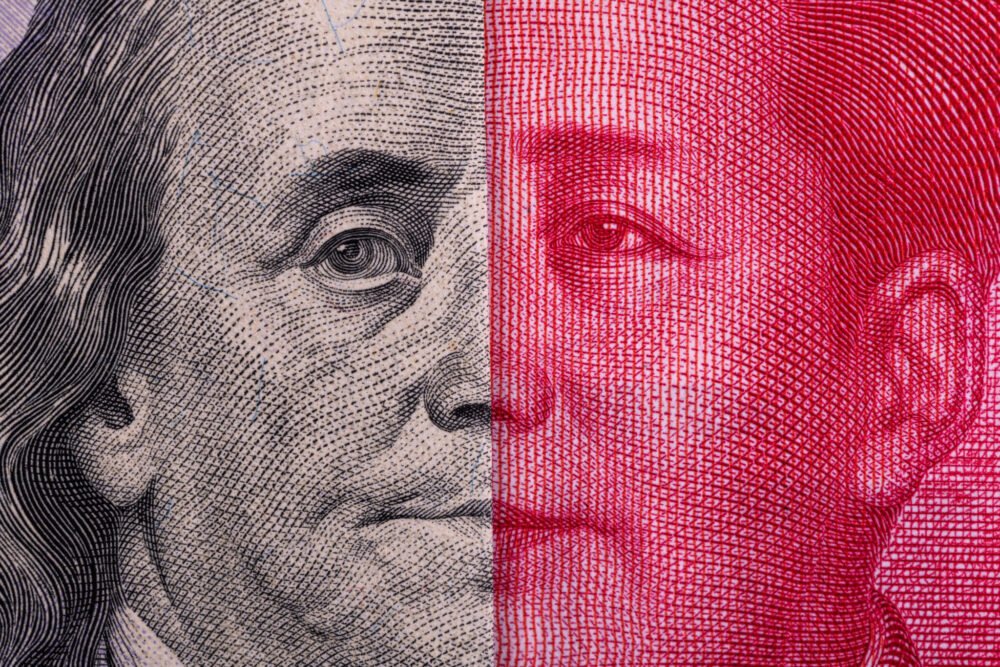

China’s Iron Ore Gambit

In a landmark move that could reshape global commodity markets and impact iron ore prices BHP Billiton has agreed to settle 30% of its iron ore spot trades with Chinese buyers in Chinese Yuan (RMB). This represents a significant departure from the longstanding U.S. dollar standard. Set to begin in Q4 2025, the shift marks a […]

Europe’s HRC Market Braces for Shock as EU Eyes Deep Quota Cuts and 50% Tariffs

Hot rolled coil prices in Europe have remained largely unchanged in the past two weeks. However, a proposal by the European Union to slash import quotas has raised concerns among market participants. Hot Rolled Coil Deliveries Surging into the EU Mills in northern Europe continue to seek €580-600 ($700) per metric ton EXW for the […]

Rare Earths Shift: Why is Australia Now The Biggest Competitor to Beat China?

While geopolitical tensions continue and rare earths supply chain vulnerabilities deepen, the United States is quietly redrawing the global map of critical mineral sourcing, and Australia seems to be emerging as a cornerstone. The latest development on this front is the U.S. Export-Import Bank (EXIM) issuing a letter of interest to fund up to US […]

Automotive MMI: Critical Mineral Restrictions Shake US Auto Supply Chains

The Automotive MMI (Monthly Metals Index) moved sideways, rising a slight 1.39%. As a whole, the US automotive market is facing a number of challenges necessitating both innovation and resilience. Why Are Critical EV Minerals in Short Supply? Automakers are grappling with shortages of critical minerals needed for electric vehicles and high-tech components. Rare earth minerals […]

Stainless MMI: Stainless Mill Hold Prices Ahead of Contracting

The Stainless Monthly Metals Index (MMI) showed little volatility during the month as all of its elements, including nickel prices, moved sideways. This translated to an overall 0.12% increase from September to October. U.S. Stainless Steel Prices, Market Holds Flat U.S. stainless prices maintained their sideways trend as mills continued the base price increases instituted […]

Will a 15% U.S. Tariff on EU Autos Reshape Global Car Trade?

In a move with major implications for the global automotive industry, the U.S. federal government has implemented a 15% import tariff on auto imports from the European Union. According to a federal register notice from September 24, the move affects cars as well as auto parts. That notice went on to indicate that the duties […]